Custodian REIT (LSE: CREI), the UK commercial real estate investment company, today reports its unaudited net asset value (“NAV”) as at 31 March 2020, highlights for the period from 1 January 2020 to 31 March 2020 (“the Period”) and an update on the impact of the COVID-19 pandemic.

The Company’s focus is on managing liquidity to mitigate the risks associated with COVID-19 disruption and maintaining a level of income for investors broadly linked to net rental receipts.

Financial highlights

- NAV total return per share[1] for the year ended 31 March 2020 (“FY20”) of 1.1% (year ended 31 March 2019 (“FY19”): 5.9%), comprising 6.2% income (FY19: 6.1%) and a 5.1% capital decrease (FY19: 0.2% capital decrease)

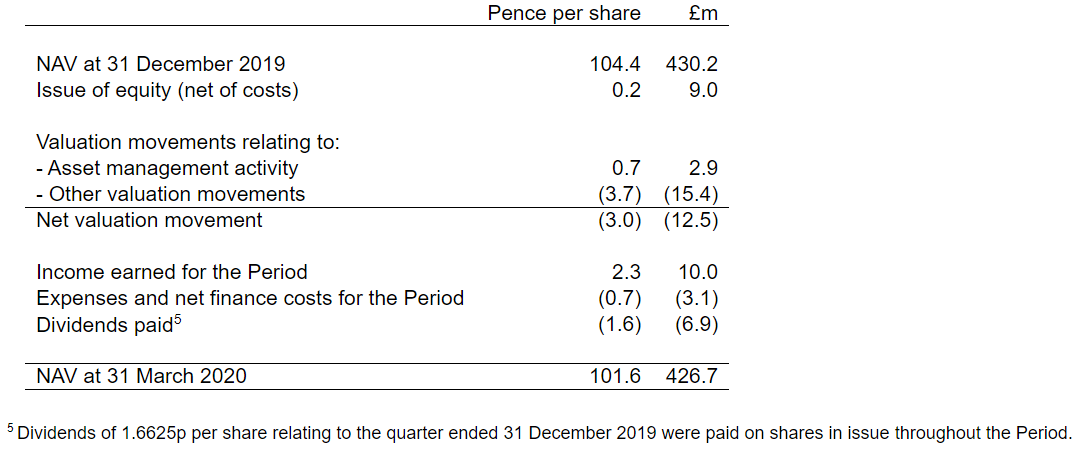

- NAV per share of 101.6p (31 December 2019: 104.4p)

- NAV of £426.7m (31 December 2019: £430.2m)

- FY20 EPRA earnings per share[2] 7.0p (FY19: 7.3p)

- Dividend per share approved for the Period of 1.6625p payable on 29 May 2020

- FY20 dividends paid and approved of 6.65p (FY19: 6.55p)

- Net gearing[3] of 22.4% loan-to-value (31 December 2019: 23.2%) comprising cash of £25m and borrowings of £150m

- £9.1m of new equity raised during the Period at an average premium of 10.6% to dividend adjusted NAV per share

- Market capitalisation of £415.9m (31 December 2019: £469.7m)

Portfolio highlights

- Property value of £559.8m (31 December 2019: £571.2m), subject to a ‘material uncertainty’ clause in line with prevailing RICS guidance

- £12.5m aggregate valuation decrease (2.2% of property portfolio) for the Period, comprising a £2.9m valuation increase from successful asset management initiatives and £15.4m decreases due primarily to the impact of COVID-19 on retail and alternative sectors

- EPRA occupancy[4] 95.9% (31 December 2019: 95.6%)

[1] NAV per share movement including dividends paid and approved for the period.

[2] Profit after tax excluding net gains on investment property divided by weighted average number of shares in issue.

[3] Gross borrowings less cash (excluding rent deposits) divided by portfolio valuation.

[4] Estimated rental value (“ERV”) of let property divided by total portfolio ERV.

Net asset value

The unaudited NAV of the Company at 31 March 2020 was £426.7m, reflecting approximately 101.6p per share, a decrease of 2.8p (2.7%) since 31 December 2019:

The NAV attributable to the ordinary shares of the Company is calculated under International Financial Reporting Standards and incorporates the independent portfolio valuation as at 31 March 2020, which is subject to a ‘material uncertainty’ clause in line with RICS guidance, and income for the Period, but does not include any provision for the approved dividend of 1.6625p per share for the Period to be paid on 29 May 2020.

COVID-19 impact

Commenting on the impact of COVID-19, Richard Shepherd-Cross, Managing Director of Custodian Capital Limited (the Company’s discretionary investment manager) said:

“The Period started with increased confidence in commercial property investment following the General Election and reduced uncertainty around Brexit. Sadly, all talk of confidence has now been eclipsed by the COVID-19 pandemic and the widespread impact on the economy in this country and globally.

“Our response has been to prioritise protecting cash flow and to secure the balance sheet. As a result the Company has withdrawn from two acquisitions of regional offices on which terms had been agreed. In addition, to address the impact of the statutory protections for commercial tenants introduced by the UK Government, the Company has agreement in principle from its lenders to put in place pre-emptive covenant waivers on interest cover[6] to provide the flexibility to collect rent in the most advantageous way for medium/long-term income security, while supporting tenants and minimising vacancies.

“It is too early to assess the long-term impact of COVID-19 on the commercial property market but we believe it may accelerate pre-existing trends in the use of, and investment in, commercial property. We expect to see a further deterioration in secondary retail, an increase in demand for flexible office space (both traditional offices, fitted out and leased flexibly, as well as serviced offices) and a continuation of the growth of logistics and distribution. As always, we would expect location to be a key determinant of the future success of commercial property assets.

“In the near-term, of even more importance than the NAV derived from current valuations is the absolute focus on rent collection, future cash flow, ongoing asset management and the affordability of future dividends which are all underpinned by the Company’s low ongoing charges ratio[7] of 1.12% and low cost of debt of 3.0% (circa £4.7m interest per annum in aggregate).”

[6] Historical rental income received less certain property expenses divided by interest payable must be greater than 250%.

[7] Expenses (excluding operating expenses of rental property recharged to tenants) divided by average quarterly NAV.

Rent collection

The Investment Manager directly manages the Custodian REIT portfolio, including rent collection, and continues to hold direct conversations with tenants regarding the payment of rent. Some of these conversations have led to positive asset management outcomes, including extending leases in return for rent concessions, providing short-term cash flow relief for occupiers and longer term income security for the Company. Importantly, at this stage, the Company has not waived or cancelled any contractual rent and all contractual rent remains due.

The Company’s rent invoicing profile comprises quarterly in advance (on both English and Scottish quarter days) and monthly in advance. Following negotiations regarding the March quarter rent, the Company has agreed that a number of tenants move from quarterly in advance to monthly in advance rent payments, or a deferral of the March quarter’s rent with a full recovery over the next 12-18 months. Some tenants have yet to agree a payment profile but the Investment Manager remains in active discussion with these tenants to agree payment plans for the balance of outstanding rent.

Given the varied profile of the Company’s rental invoicing, the Board believes reporting rent collected relating to the month of April best reflects the prevailing level of income generation from the Company’s property portfolio. To date, 74% of rent contractually due relating to the month of April[8] has been collected and 14% has been deferred by agreement (and is therefore no longer due in April) to be paid either monthly in arrears or to be recovered through a payment plan over the next 12-18 months.

[8] Comprising payments received relating to April 2020 from: Scottish quarterly invoicing in advance in February 2020, English quarterly invoicing in advance in March 2020 and monthly invoicing in advance in April 2020.

Asset management

Despite the uncertainty caused by COVID-19, the Investment Manager has remained focused on active asset management including rent reviews, new lettings, lease extensions and the retention of tenants beyond their contractual break clauses during the Period, completing:

- An outstanding rent review with JTF Wholesale on a trade counter in Warrington, increasing passing rent by 20% to £586k, adding £0.9m to valuation;

- A 10 year reversionary lease with five year break option with VP Packaging on an industrial unit at Venture Park, Kettering, with fixed rental increases which over time will increase passing rent by more than 20%, increasing valuation by £0.5m;

- A five year reversionary lease with Vertiv Infrastructure on an industrial unit at Priory Business Park, Bedford, extending the lease to August 2027 and increasing the valuation by £0.4m;

- A new 10 year reversionary lease with Arkote on an industrial unit in Sheffield, extending the lease to February 2034 and increasing the valuation by £0.2m;

- A five year lease renewal with Wienerberger on offices at Cheadle Royal Business Park with expiry now in March 2025 and rent increasing by 10%, increasing the valuation by £0.2m;

- A five year lease renewal with a 2.5 year tenant only break option with Poundland on a high street retail unit in Portsmouth, with rent decreasing by 50% to match the ERV, increasing the valuation by £0.2m;

- A five year lease renewal with a 2.5 year tenant only break option with DHL on an industrial unit at Glasgow Airport, with rent increasing by 17% and valuation increasing by £0.2m;

- A 10 year lease with five year break to Raven Valley on an industrial unit at Metro Riverside in Gateshead at a passing rent of £52k per annum in line with ERV, increasing the valuation by £0.2m; and

- A five year lease renewal with Holland & Barrett on a high street retail unit in Shrewsbury with passing rent decreasing by 25% to £75k per annum in line with ERV, increasing valuation by £0.1m.

These positive asset management outcomes have been offset by Laura Ashley entering administration, which is expected to result in lost annual contractual rent of £0.23m in total from the Company’s Grantham and Colchester assets.

The portfolio’s weighted average unexpired lease term to first break or expiry (“WAULT”) decreased from 5.4 years at 31 December 2019 to 5.3 years at the Period end, reflecting the natural elapse of time largely offset by the successful asset management initiatives above.

Financial resilience

The Company retains its strong financial position to address the extraordinary circumstances imposed by COVID-19, having:

- A diverse and high-quality asset and tenant base comprising 161 assets and over 250 typically ‘institutional grade’ tenants across all commercial sectors, with an occupancy rate of 95.9%;

- £25m of cash-in-hand with gross borrowings of £150m resulting in low net gearing, with no short-term refinancing risk and a weighted average debt facility maturity of seven years; and

- Significant headroom on lender covenants at a portfolio level, with Company net gearing of 22.4% compared to a maximum loan to value (“LTV”) covenant of 35%.

The Company operates the following loan facilities:

- A £50m revolving credit facility (“RCF”) with Lloyds Bank plc (“Lloyds”) expiring on 17 September 2022 with interest of between 1.5% and 1.8% above three-month LIBOR, determined by reference to the prevailing LTV ratio of a discrete security pool. The RCF is currently £35m drawn;

- A £20m term loan with Scottish Widows plc (“SWIP”) repayable on 13 August 2025 with interest fixed at 3.935%;

- A £45m term loan with SWIP repayable on 5 June 2028 with interest fixed at 2.987%; and

- A £50m term loan with Aviva Investors Real Estate Finance (“Aviva”) comprising:

- A £35m tranche repayable on 6 April 2032 with fixed annual interest of 3.02%; and

- A £15m tranche repayable on 3 November 2032 with fixed annual interest of 3.26%.

Each facility has a discrete security pool, comprising a number of the Company’s individual properties, over which the relevant lender has security and covenants:

- The maximum LTV of the discrete security pool is between 45% and 50%, with an overarching covenant on the Company’s property portfolio of a maximum 35% LTV; and

- Historical interest cover, requiring net rental receipts from each discrete security pool, over the preceding three months, to exceed 250% of the facility’s quarterly interest liability.

The Company has £184.8m (33% of the property portfolio) of unencumbered assets which could be charged to the security pools to enhance the LTV on the individual loans.

At a portfolio level, the aggregate interest cover on borrowings was more than 600% for the quarter ended 31 March 2020. However, interest cover covenants on individual facilities may come under some short-term pressure due to anticipated curtailed rental receipts. To mitigate this risk, the Company has agreement in principle from its lenders to put in place pre-emptive covenant waivers on interest cover for the next two quarters in return for depositing amounts equivalent to interest payable for that period into charged accounts.

Portfolio analysis

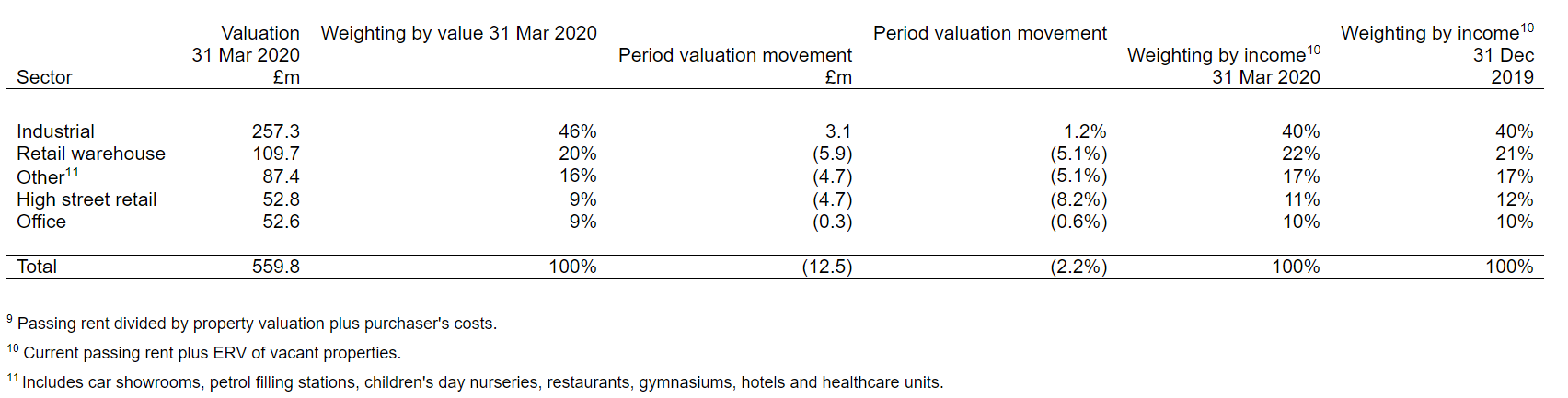

At 31 March 2020 the Company’s property portfolio comprised 161 assets with a net initial yield[9] (“NIY”) of 6.8% (31 December 2019: 6.6%). The portfolio is split between the main commercial property sectors, in line with the Company’s objective to maintain a suitably balanced investment portfolio. Sector weightings are shown below:

During the Period we have experienced a net decline in the portfolio valuation that broadly reflects the market trends in the differing sectors. Industrial and logistics values have marginally strengthened by 1.2%, office values have been broadly flat and we have seen a decline in retail values with a greater percentage decline in high street locations (8.2%) compared to out of town retail warehousing (5.1%). This is perhaps a reflection of the stock selection in the Custodian REIT portfolio where retail warehouse occupiers are predominantly value retailers and homewares/DIY, many of whom have remained open for trading during the lockdown, even if at restricted levels. Furthermore, the average rent across the retail warehouse portfolio is only £14.31 per square foot, which represents an affordable rent for most occupiers.

The valuation is reported on the basis of ‘material valuation uncertainty’ as per the current RICS valuation standards. This does not invalidate the valuation but, in the current extraordinary circumstances, implies that less certainty can be attached to the valuation than otherwise would be the case. There is a body of market evidence to support the valuations in the usual way but, in addition, the valuers have reflected market sentiment in their reported numbers.

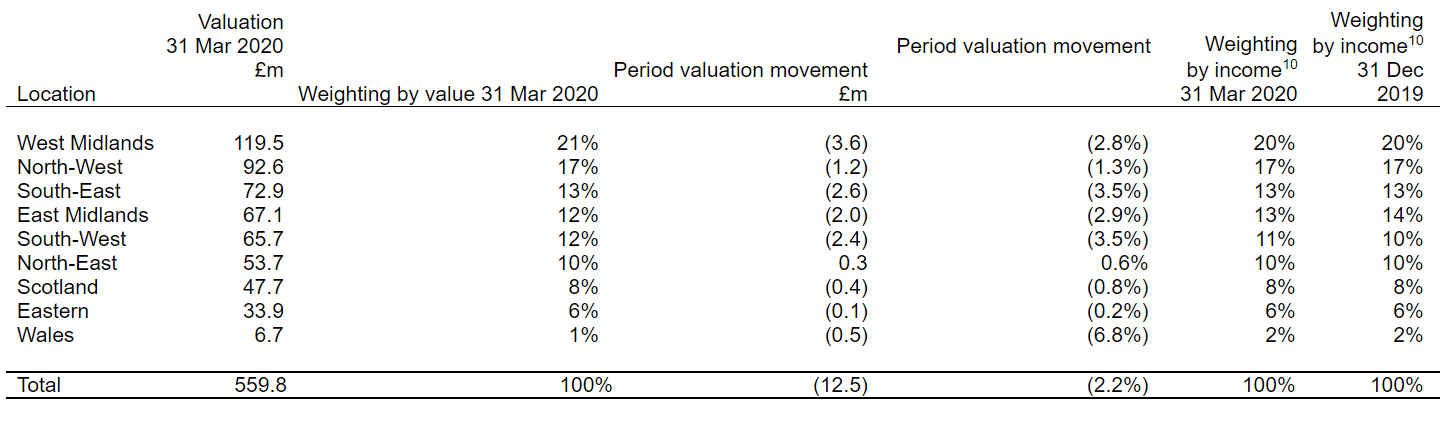

The Company operates a geographically diversified property portfolio across the UK, seeking to ensure that no one region represents an overweight position. The geographic analysis of the Company’s portfolio at 31 March 2020 was as follows:

For details of all properties in the portfolio please see www.custodianreit.com/property-portfolio.

Equity

The Company issued 8.0m new ordinary shares of 1p each (“the New Shares”) during the Period raising £9.1m. The New Shares were issued at a premium of 10.6% to the unaudited NAV per share at 31 December 2019, adjusted to exclude the dividend paid on 28 February 2020.

Dividends

The Board intends to make the fourth quarterly interim dividend payment relating to the Period of 1.6625p per share on 29 May 2020, reflecting the normal collection of rent for the quarter ended 31 March 2020, and consequently meeting its target of paying an annual dividend per share for the financial year of 6.65p (2019: 6.55p).

However, as explained earlier, we are experiencing an inevitable disruption to cash collection in the current quarter, due to the COVID-19 pandemic, as a number of tenants seek to defer rental payments to protect their own cash flows. As a result, the current level of dividend is not expected to be fully supported by net rental receipts while the COVID-19 pandemic is impacting rent collections.

Acknowledging the importance of income for shareholders, the Company intends to pay the next two quarterly dividends at a minimum of 0.75p per share[12], regardless of rent collection rates. Should rent collections in June and September quarters allow, more generous dividends may be possible. Over the course of the financial year, as deferred rents are collected, the Board hopes it will be possible to restore the dividend to a sustainable long-term level akin to previous years.

[12] This is a target only and not a profit forecast. There can be no assurance that the target can or will be met and it should not be taken as an indication of the Company’s expected or actual future results. Accordingly, shareholders or potential investors in the Company should not place any reliance on this target in deciding whether or not to invest in the Company or assume that the Company will make any distributions at all and should decide for themselves whether or not the target dividend yield is reasonable or achievable.