Custodian REIT (LSE: CREI), the UK commercial real estate investment company, today reports its final results for the year ended 31 March 2018.

Financial highlights and performance summary

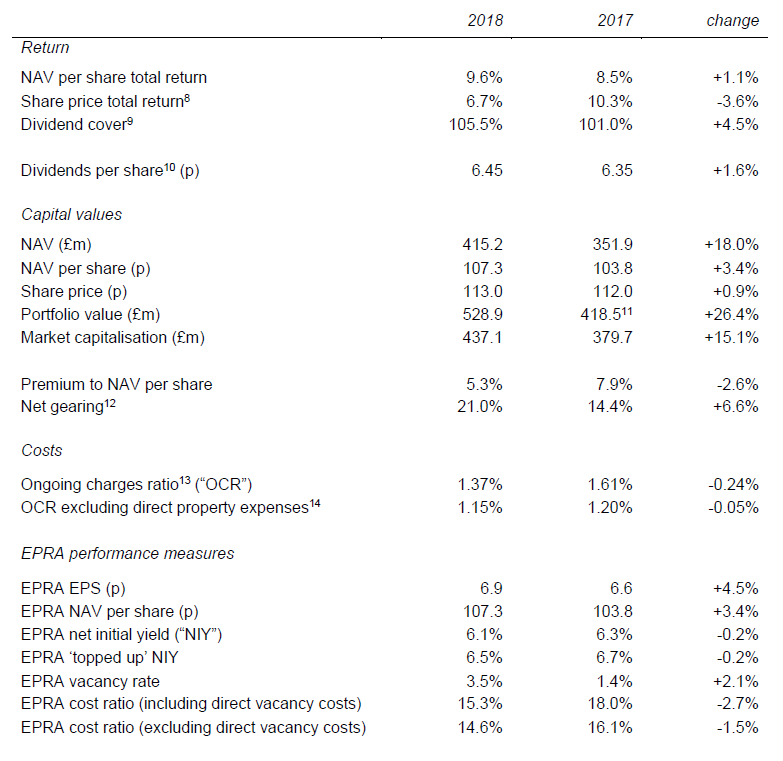

- NAV per share total return¹ of 9.6% (2017: 8.5%)

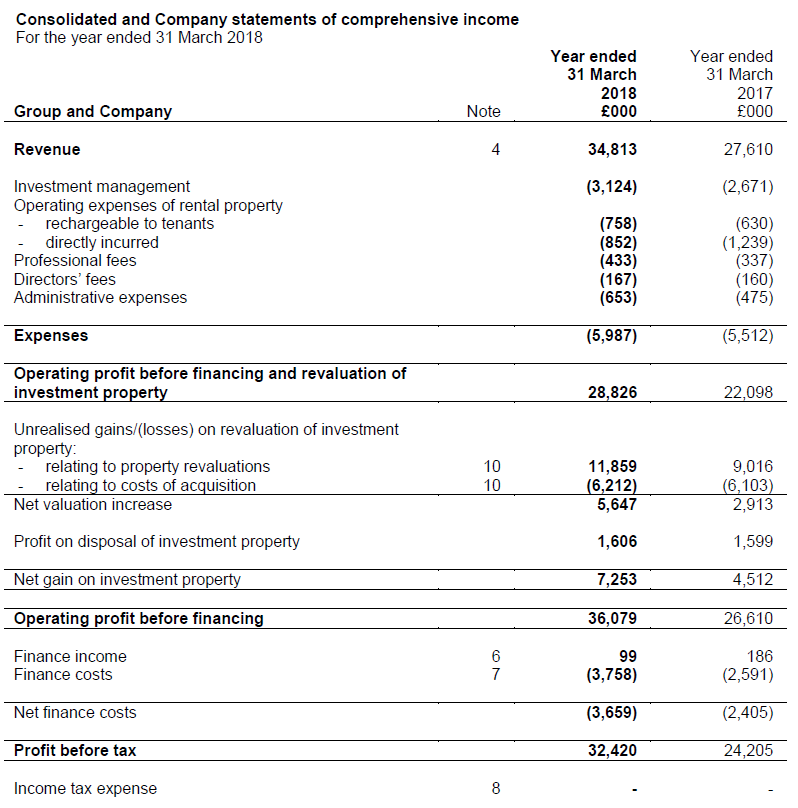

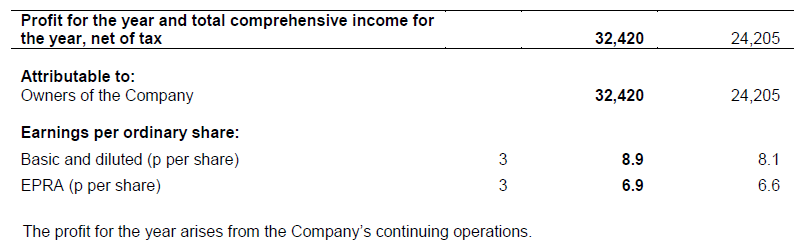

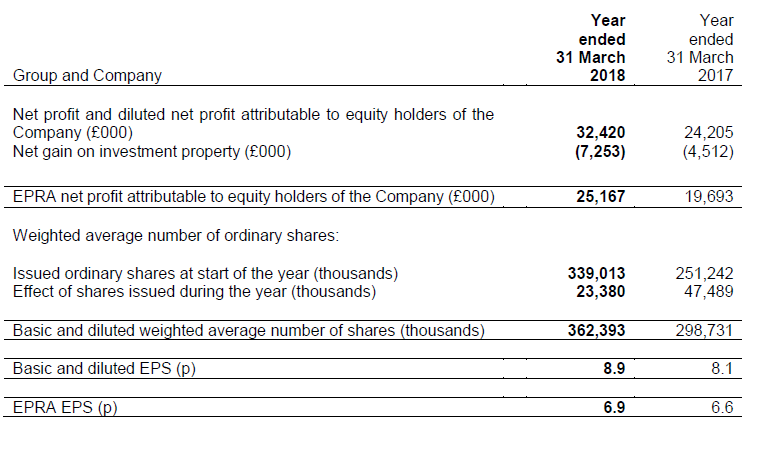

- EPRA² earnings per share³ of 6.9p (2017: 6.6p), basic and diluted earnings per share of 8.9p (2017: 8.1p)

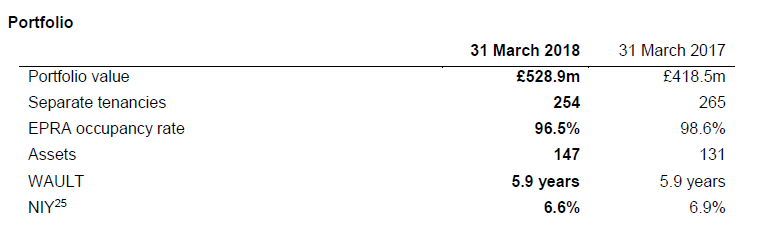

- Portfolio value of £528.9m (2017: £418.5m⁴)

- Profit after tax up 34% to £32.4m (2017: £24.2m)

- £54.7m⁵ of new equity raised at average premium of 11.1% to dividend adjusted NAV

- 2019 target dividend per share increased to 6.55p (2018: 6.45p)

- £106.3m⁶ invested in 20 acquisitions, one ongoing pre-let development and one significant refurbishment

- £8.8m valuation uplift from successful asset management initiatives, £5.7m net valuation increase⁷

- £1.6m profit on disposal of five properties for an aggregate consideration of £11.3m

Alternative performance measures, including EPRA Best Practice Recommendations, are among the key performance indicators used by the Board to assess the Company’s performance. EPRA performance measures have been disclosed to facilitate comparison with the Company’s peers through consistent reporting of key performance measures. The Company is a FTSE EPRA/NAREIT index series constituent.

Commenting on the final results, David Hunter, Chairman of Custodian REIT, said:

“I am pleased to report that Custodian REIT has continued to deliver strong shareholder returns with NAV per share total return of 9.6% (2017: 8.5%) for the year. We invested a total of £106.3m on the completion of 20 acquisitions, one ongoing pre-let development and one significant refurbishment, funded principally by £54.7m raised from the issue of new shares and £50.0m of new term debt.

“We believe a well-defined investment strategy that offers secure income and focuses on long-term goals and deliverable targets will protect shareholders from market volatility.

“The strength of the occupational market represents an exciting opportunity and rental growth at lease renewal and rent review remains robust. The Company met its target of paying an annual dividend per share for the year of 6.45p (2017: 6.35p, 2016: 6.25p), 105.5% covered by net recurring income, and we expect proactive asset management that secures rental growth will continue to drive performance in the portfolio. We are confident we can maintain occupancy levels, which in turn will sustain our policy of paying a growing and fully-covered dividend to shareholders.”

Further information

Further information regarding the Company can be found at the Company’s website www.custodianreit.com or please contact:

Custodian Capital Limited

Richard Shepherd-Cross / Nathan Imlach / Ian Mattioli MBE

Tel: +44 (0)116 240 8740

www.custodiancapital.com

Numis Securities Limited

Hugh Jonathan / Nathan Brown

Tel: +44 (0)20 7260 1000

www.numiscorp.com

Camarco

Hazel Stevenson

Tel: +44 (0)20 3757 4989

www.camarco.co.uk

Chairman’s statement

I am pleased to report that Custodian REIT has continued to deliver strong shareholder returns with NAV per share total return of 9.6% (2017: 8.5%) for the year ended 31 March 2018. During the year we invested a total of £106.3m on the completion of 20 acquisitions, one ongoing pre-let development and one significant refurbishment, funded principally by £54.7m raised from the issue of new shares and £50.0m of new term debt. Increasing the scale of the Company and a continued focus on controlling costs has reduced the ongoing charges ratio (excluding direct property expenses) from 1.20% to 1.15%. We plan to achieve continued growth to realise the further economies of scale offered by the Company’s relatively fixed cost base and the reduced rate of Investment Manager fees from 1 June 2017, while adhering to the Company’s investment policy and maintaining the quality of both properties and income.

The Company pays one of the highest fully covered dividends amongst its peer group of listed property investment companies¹⁵. During a period of further growth we have sought to minimise the impact of ‘cash drag’ following the issue of new shares by taking advantage of the flexibility offered by the Company’s £35.0m revolving credit facility (“RCF”). I am delighted that proactive asset management of the portfolio to secure rental growth, coupled with the flexibility of the RCF and prompt deployment of cash as it has been raised through equity issuance, has allowed us to increase the target dividend¹⁶ for the year ending 31 March 2019 by 1.6% to 6.55p per share.

Through 2017 and into the first quarter of 2018 the market has been characterised by a very restricted supply of investment opportunities and a significant level of demand from a range of investors. Market demand has polarised, moving away from high street retail and focusing on industrial/logistics assets and properties let on long leases, particularly those with rents indexed to inflation. We believe the market is over-pricing some assets and we have taken a cautious approach to acquisitions. Custodian REIT has stuck firmly to its investment strategy making it more difficult, but not impossible, to deploy our available resources into the right property assets. Despite our success in investing more than £100m during the year, these market conditions have restricted our ability to satisfy demand for new equity issuance which in turn has seen the Company’s shares trade at a premium well ahead of most of our peers. Current market dynamics look likely to persist and maintain the status quo for the rest of the year.

Custodian REIT remains focused on good quality regional property that might be considered too small for institutional investors. The Company continues to maintain a diverse portfolio strategy, allowing enough flexibility to be contracyclical where appropriate but always with a strong focus on acquiring assets that support the dividend policy of the Company. Furthermore, we believe a well-defined investment strategy that offers secure income and focuses on long-term goals and deliverable targets will protect shareholders from market volatility.

Net asset value

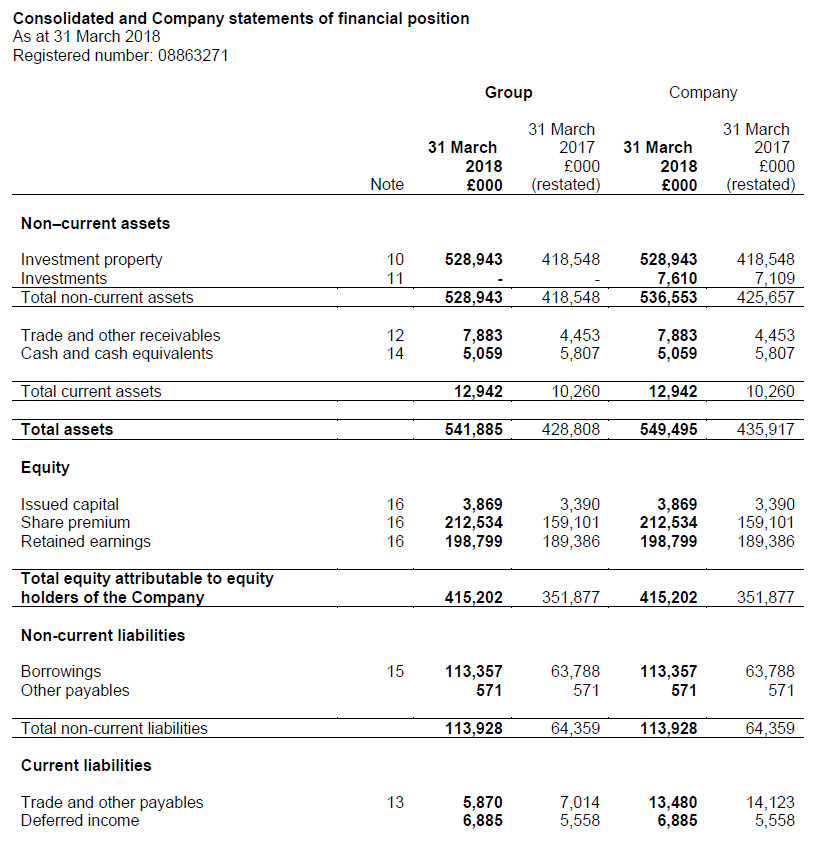

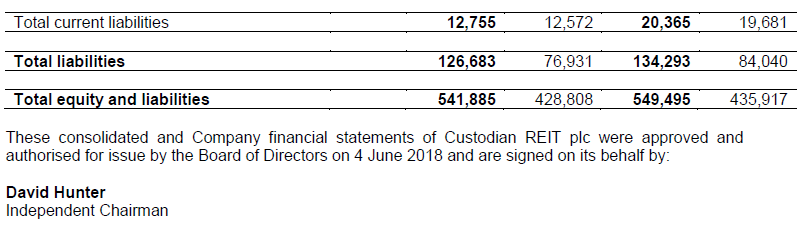

The NAV of the Company at 31 March 2018 was £415.2m, reflecting approximately 107.3p per share, an increase of 3.4% since 31 March 2017:

The Company delivered NAV per share total return of 9.6% for the year, which was another period of significant new investment where the initial costs (primarily stamp duty) of investing £106.3m in 20 property acquisitions, one pre-let development and one significant refurbishment diluted NAV per share total return by circa 1.6p, largely offset by raising £53.9m of new equity (net of costs) at an average 11.1% premium to dividend adjusted NAV, which added 1.5p per share¹⁸ and fully covered the cost of raising and deploying the proceeds.

In addition to acquisitions, activity during the year also focused on pro-active asset management, which generated an £8.8m valuation uplift. We intend to continue our asset management activities and complete the current acquisition pipeline where we have identified compelling propositions, with the deployment of existing debt facilities expected to increase net gearing towards our target level of 25% loan-to-value (“LTV”).

Share price

Consistent demand for the Company’s shares has led to its share price showing a relatively stable premium to NAV through the year.

This share price performance has been combined with a steadily increasing level of daily liquidity which now rates Custodian REIT as the second highest in its peer group in terms of volume of shares traded daily as a percentage of issued share capital¹⁹. This liquidity has done much to reduce volatility so the few instances of short-term share price volatility have quickly stabilised.

The Company enjoys the support of a wide range of shareholders with the majority classified as private client or discretionary wealth management investors. The Company’s investment and dividend strategy is very well suited to investors looking for a close proxy to direct real estate but in a managed and liquid structure. The nature of shareholders has, in turn, helped to reduce volatility as they are typically long-term holders looking for stable dividend-driven returns.

Placing of new ordinary shares

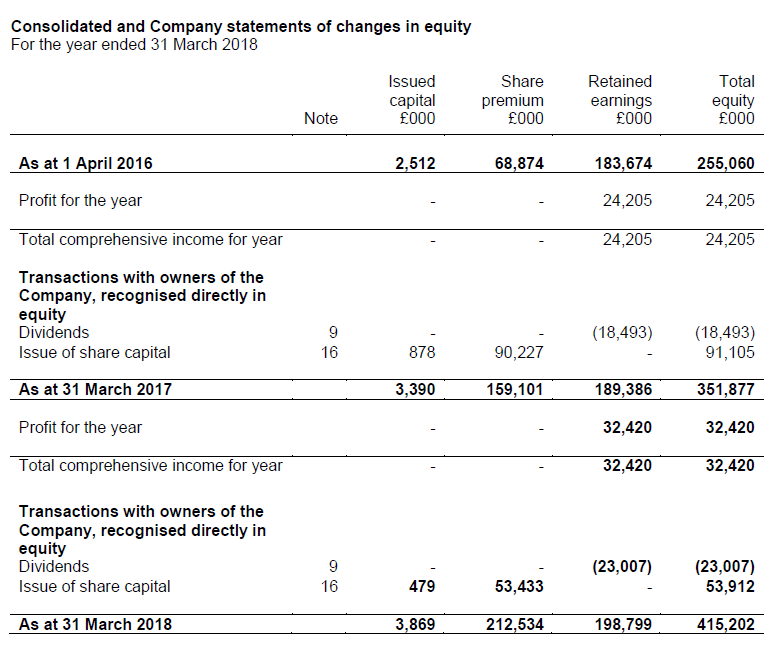

The Company raised £54.7m of new equity during the year, placing 47.8m new shares at an average 11.1% (2017: 5.1%) premium to dividend adjusted NAV via an ongoing programme of tap issuance.

Borrowings

As at 31 March 2018 net gearing equated to 21.0% LTV. The Board’s strategy is to:

- Increase debt facilities in line with portfolio growth, targeting net gearing of 25% LTV;

- Facilitate expansion of the portfolio to take advantage of expected rental growth; and

- Reduce shareholders’ exposure to risk by:

- Taking advantage of low interest rates to secure long-term, fixed rate borrowing; and

- Managing the weighted average maturity (“WAM”) of the Company’s debt facilities.

To achieve these objectives, on 5 April 2017, the Company and Aviva Investors Real Estate Finance (“Aviva”) entered into an agreement for Aviva to provide the Company with a new 15 year £50m term loan facility, comprising two tranches of £35m (“Tranche 1”) and £15m (“Tranche 2”) respectively. The Company drew down Tranche 1 on 6 April 2017, with a fixed rate of interest of 3.02% per annum, and drew down Tranche 2 on 3 November 2017 with a fixed rate of interest of 3.26% per annum.

The weighted average cost of the Company’s agreed debt facilities at 31 March 2018 was 3.1% (2017: 3.1%) with a WAM of 9.1 years (2017: 10.1 years) and 77% (2017: 77%) of the Company’s agreed debt facilities now at a fixed rate of interest. This removes significant interest rate risk from the Company and provides shareholders with a wide, beneficial margin between the fixed cost of debt and income returns from the portfolio.

Investment Manager

Custodian Capital Limited (“the Investment Manager”) was appointed at IPO under an investment management agreement (“IMA”) to provide property management and administrative services to the Company. The performance of the Investment Manager is reviewed each year by the Management Engagement Committee (“MEC”).

The Board is pleased with the performance of the Investment Manager, particularly the timely deployment of new monies on high quality assets, securing the earnings required to fully cover the target dividend, and the asset management successes.

On 1 June 2017, the Investment Manager was appointed for a further three years and fees payable to the Investment Manager under the IMA were amended to include:

- A step down in the property management fee from 0.75% to 0.65% of NAV applied to NAV in excess of £500m; and

- A step down in the administrative fee from 0.125% to 0.08% of NAV applied to NAV between £200m and £500m and a further step down to 0.05% of NAV applied to NAV in excess of £500m.

These amendments to the IMA secured an immediate reduction in the administrative fee rate, increasing cover on target dividends in the current and future years. Further growth in NAV, particularly above £500m, will further reduce the Company’s ongoing charges ratio and increase dividend capacity.

WAULT

The Investment Manager’s report sets out in detail a proposed change to the Company’s investment policy regarding weighted average unexpired lease term to the earlier of first break or expiry (“WAULT”).

With the natural passage of time and the growth in size of the portfolio, as well as the general market overpricing of many longer lease assets, the target of maintaining a portfolio WAULT of more than five years is now inappropriate. It is proposed that this be changed to a more realistic objective to minimise rental voids and enhance the WAULT of the portfolio by managing lease expiries and targeting property acquisitions which will in aggregate be accretive to WAULT at the point of acquisition, on a rolling 12-month basis. The Board fully supports this change which will provide the Investment Manager with additional flexibility when looking for the best value properties to add to the portfolio.

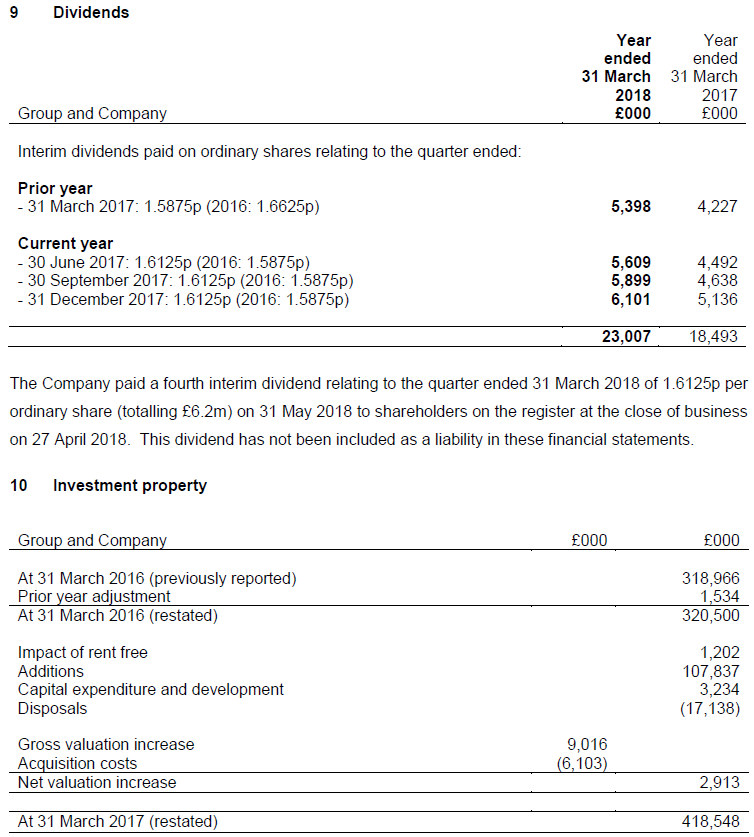

Dividends

Income is a major component of total return. The Company paid aggregate dividends of 6.425p per share during the year (totalling £23.0m), comprising the fourth interim dividend of 1.5875p per share relating to the year ended 31 March 2017 and three interim dividends of 1.6125p per share relating to the year ended 31 March 2018.

The Company paid an interim dividend of 1.6125p per share for the quarter ended 31 March 2018 on 31 May 2018, meeting the Company’s target of paying an annual dividend per share relating to the year of 6.45p (2017: 6.35p, 2016: 6.25p), totalling £23.8m. Dividends relating to the year are 105.5% covered by net recurring income of £25.2m.

In the absence of unforeseen circumstances, the Board intends to pay quarterly interim dividends to achieve a target dividend of 6.55p per share for the year ending 31 March 2019. The Board’s objective is to grow the dividend on a sustainable basis at a rate which is fully covered by projected net rental income and does not inhibit the flexibility of the Company’s investment strategy.

Outlook

Notwithstanding our cautious approach to investment in the current market we believe that value can still be found with a disciplined approach to deployment with the strength of the occupational market representing an exciting opportunity which is discussed more fully in the Investment Manager’s report. Rental growth at lease renewal and rent review remains robust. We expect proactive asset management and rental growth will continue to drive performance in the portfolio and are confident we can maintain occupancy levels, which in turn will sustain our policy of paying a growing and fully-covered dividend to shareholders.

David Hunter

Independent Chairman

4 June 2018

Investment Manager’s report

The UK property market

Our review of the UK property market shows demand is outstripping supply in almost all sectors save for secondary retail. In November 2017 Property Week reported that allocations to commercial property now exceed 10% in global institutional portfolios, up from 8.9% in 2013. While a small percentage increase, the absolute impact has been significant resulting in competition for acquisitions as most participants in the commercial property market are targeting net investment across their portfolios. Is this a positive endorsement of the UK property investment market or is it looking like a late cycle bubble?

Last year I commented as follows: “We are not unduly concerned by this risk. The equivalent yield²⁰ of the portfolio has been constant at c. 6.75% since 2014, although the NIY of the portfolio has hardened to reflect rental growth. This suggests that capital growth has been driven by the prospect of rental growth and not by underlying yield compression, lessening the risk of a reversal of gains made in the near future.”

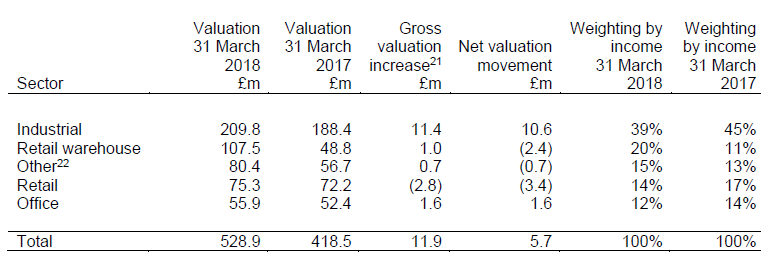

A year on we have witnessed some equivalent yield compression in our valuations, principally driven by market pricing for industrial and logistics assets, which make up 39% of the portfolio, but we have also seen softening in pricing for high street retail which makes up only 14% of the portfolio. The net result has been an increase in the valuation of the portfolio, which we still believe is robust, showing a NIY of 6.6%. Furthermore, the aggregate NIY of the £103.8m of property acquisitions during the year was 6.7% which compares favourably to Lambert Smith Hampton’s recently reported all property transaction yield of 5.67% for Q1 2018. This demonstrates that it is still possible to find properties that support Custodian REIT’s attractive, fully covered dividend policy, but it is safe to say it is somewhat harder than 12 months ago. While we are not concerned that the Custodian REIT portfolio is in a late cycle bubble, we are not immune from the market.

The first point to note is that the property market is very different: In 2007/2008 we were at the tail end of a debt driven, development boom which had left us with an over-supply of vacant property; we were at the end of rental growth cycle; we had debt fueled investment demand; interest rates were 5% and we were on the brink of a global banking collapse.

Current market conditions are somewhat different. We have had very low levels of development for 10 years and still there is very limited banking support for speculative development, leaving us with low levels of modern vacant real estate; rental growth may have peaked or even be declining in central London but in regional markets it is a different picture. Industrial and office rents have been growing since 2016 and while the rate of growth may be slowing there remain a large number of regional assets with latent rental growth. Investment demand is principally driven by equity rather than debt, although the low cost of finance is enhancing demand; interest rates are 0.5% and while we believe the Bank of England wishes to raise rates we envisage a medium term low rate environment, notwithstanding some small increases; and while we do not fear a banking crisis, we have the uncertainty of leaving the EU next year instead. The jury may be out on the outcome for UK plc of leaving the EU but we are hopeful that the impact on UK commercial property investment might be less than for those invested in assets directly linked to financial markets. Perhaps the current allocations to UK property support this view.

So even though the market backdrop is very different to 2007/2008, some investor activity has some of the hallmarks of a late cycle bubble. There seems to be a core of investors intent on deploying capital into the UK property market at any cost and some pricing reflects this. The hope of any market facing a bursting bubble is for a soft landing. We feel confident that the current occupational market dynamics and the low return environment will secure a soft landing for commercial property if one is needed.

Occupational market

Strength in occupational markets has supported much of our asset management activities throughout the year. We have settled 17 rent reviews showing increases ranging from 2% to 87% with an 18% average adding £0.5m to the Company’s rent roll. While much of the growth has come from the industrial sector, with 12 rent reviews, there has also been growth in other sectors with three retail rental uplifts and two alternative assets.

There remain a number of factors that should lead to a continuing period of rental growth:

- 2008-2016 saw rental levels in many regional markets fall in nominal terms against a background of annual economic inflation averaging c. 3% per annum, leading to like-for-like rental declines of 20-25%. As a result rents are now growing from a low and affordable base in real terms.

- Many regional markets are witnessing rental levels which remain below the threshold necessary to bring forward new development. This is a function of the fall in real rental levels against inflation in construction and labour costs. It would appear that there is a latent pool of rental growth on which the market must deliver before we see supply reach equilibrium with demand, thus maintaining pressure on rents to grow.

- Many tenant negotiations remain finely balanced, with tenants keenly aware of their value to landlords. However tenants are accepting of rental growth, which they may have avoided for as much as 10 years in many instances, which combined with limited supply of alternative premises, should continue to deliver rental growth albeit at a lessening rate.

In addition, 13% of the Company’s rent roll benefits from fixed or indexed rental uplifts, although there is increasingly strong evidence of open market rental growth matching or exceeding indexation.

However we have seen some weakness in secondary retail locations and expect to experience one or two rental reductions at lease expiry. Some tenants have taken matters into their own hands to bring about early rental reductions with the aggressive use of company voluntary arrangements (“CVAs”) to step away from their lease obligations or to reduce rents. Happily we have been largely unaffected by this. We have no exposure to House of Fraser or New Look and the lease over our restaurant let to Prezzo was assigned in advance of its CVA so we were unaffected, but Carpetright’s CVA has resulted in a 25% reduction in rent at our Grantham store (a £25k drop in rent representing 0.07% of the Company’s rent roll). This is perhaps where Custodian REIT has the greatest protection against the impact of CVAs or other tenant failure, as the Company’s largest tenant represents only 3.2% of the total rent roll and with 201 tenants any instance of tenant default will have only a muted impact on the Company.

Investment objective

The Company’s key objective is to provide shareholders with an attractive level of income by maintaining the high level of dividend, fully covered by earnings, with a conservative level of net gearing. We are delighted to have continued to achieve this, with earnings providing 105.5% cover of the approved total dividend relating to the year of 6.45p per share, with a net gearing ratio of 21.0% at the year end. As a result of the fund’s growth and consequential reduction in OCR the Board has increased the target dividend for the next financial year to 6.55p per share.

We continue to pursue a pipeline of new investment opportunities with the aim of deploying the Company’s undrawn debt facilities up to the conservative net gearing target of 25% LTV. At the current cost of debt, we believe this strategy can improve dividend cover as net gearing increases towards the target level.

We remain committed to a strategy principally focused on sub £10m lot size regional property. We expect to see continuing strong asset management performance as we secure rental increases and extend contractual income.

Portfolio balance

The portfolio is split between the main commercial property sectors, in line with the Company’s objective to maintain a suitably balanced investment portfolio, with a relatively low exposure to office and a relatively high exposure to industrial, retail warehouse and alternative sectors, often referred to as ‘other’ in property market analysis. The current sector weightings are:

Industrial property is a very good fit with the Company’s strategy where it is possible to acquire modern, ‘fit-for-purpose’ buildings with high residual values (ie the vacant possession value is closer to the investment value than in other sectors) and where the real estate is less exposed to obsolescence. £5.9m of the £11.4m gross valuation increase in the industrial sector was driven by asset management initiatives, with occupational demand driving rental growth and generating positive returns.

There is continued weakness in secondary high street retail locations, with rental levels still under pressure and a very real threat of vacancy. However, the high street is a polarised sector where many locations continue to be in demand by retailers. We will continue to rebalance the portfolio to focus on strong retail locations while working on an orderly disposal of those assets we believe are ex-growth. The current well-publicised crop of CVAs has the potential to increase vacancy levels in our retail warehousing portfolio, but set against a backdrop of very low vacancy rates in this sector we do not feel unduly exposed to long-term void risk.

While deemed to be outside the core sectors of office, retail and industrial the ‘other’ sector offers diversification of income without adding to portfolio risk, containing assets considered mainstream but which typically have not been owned by institutional investors. The ‘other’ sector continues to be a target for acquisitions.

Office rents in regional markets are growing and supply remains constrained by a lack of development and the extensive conversion of secondary offices to residential making returns very attractive. However, we are conscious that obsolescence and lease incentives can be a real cost of office ownership, which can hit cash flow and be at odds with the Company’s relatively high target dividend, so while we are experiencing rental growth in our office portfolio, we remain a cautious investor.

For details of all properties in the portfolio please see www.custodianreit.com/property/portfolio.

WAULT

During the year we proactively managed the portfolio, enhancing income and maintaining the WAULT ahead of the Company’s objective of a WAULT of over five years.

At 31 March 2018 the portfolio’s WAULT was 5.9 years (2017: 5.9 years) with the completion of asset management initiatives and acquisitions with an aggregate WAULT of 8.5 years offsetting the one year decline due to the passage of time.

WAULT is a much-quoted statistic and is often considered a proxy for risk. This perception has encouraged many investors to pursue long-dated income causing significant price inflation for long lease assets. Although buying shorter leases puts pressure on the WAULT of the portfolio, we believe that with the current strength of the occupational market and a portfolio of high quality properties, risk is better managed by pursuing a strategy of buying high quality properties that are likely to re-let, rather than highly priced properties with long leases. This view, combined with the growth in size of the portfolio means we believe the target of maintaining a portfolio WAULT of more than five years is inappropriate, and we have recommended to the Board that shareholders approve amending the Company’s investment objective at the Annual General Meeting (“AGM”) on 19 July 2018 as follows:

- Current WAULT policy: The Company will seek to maintain a WAULT of over five years across the portfolio secured against low risk tenants and to minimise rental voids.

- Proposed WAULT policy: The Company will seek to minimise rental voids and enhance the WAULT of the portfolio by managing lease expiries and targeting property acquisitions which will in aggregate be accretive to WAULT at the point of acquisition, on a rolling 12-month basis.

Asset management

Successful asset management strategies including rent reviews, new lettings, lease extensions and the retention of tenants beyond their contractual break clauses have more than offset the impact on NAV of acquisition costs. In aggregate asset management activities increased NAV by £8.8m delivering the largest component of NAV performance through the year. This element of NAV growth underlines the importance of pro-active, strategic asset management of the portfolio. As a fund manager who collects rent and has direct relationships with all the tenants in the portfolio, we have been able to deliver mutually beneficial outcomes for both the Company and its tenants.

Key asset management initiatives completed during the year included:

Finalising a rent review in Southwark, increasing annual rent by 87% from £0.20m pa (£9 per sq ft) to £0.37m pa (£16.25 per sq ft), exceeding ERV of £0.27m pa (£12 per sq ft) and increasing valuation by £2.5m;

- Agreeing a new 10-year lease with Regus in West Malling, increasing annual rent by 14.5% from £0.56m pa (£19.20 per sq ft) to £0.64m pa (£22 per sq ft) and increasing valuation by £2.4m;

- Agreeing a rent review at £0.33m per annum and a five-year reversionary lease with YESSS Electrical at Foxbridge Way, Normanton, increasing valuation by £1.0m;

- Finalising a rent review with DHL in Warrington at £0.31m per annum, increasing valuation by £0.6m;

- Settling a rent review with the tenant at Leacroft Road, Warrington and assigning the lease to a larger group entity with a stronger covenant, increasing valuation by £0.5m;

- Letting a vacant unit in Gateshead to WH Partnership on a 10-year lease at £0.14m per annum, increasing valuation by £0.4m;

- Agreeing a new 10-year reversionary lease with Powder Systems at Estuary Commerce Park, Speke with expiry moving from July 2020 to July 2030 and annual rent increasing by 7% from £0.14m to £0.15m, increasing valuation by £0.4m;

- Assigning the lease at Ravensbank Drive, Redditch to a larger group entity with a stronger covenant, increasing valuation by £0.3m;

- Removing an August 2018 break clause in Bunzl’s lease in Castleford increasing WAULT from 1.2 years to 6.2 years, increasing valuation by £0.2m;

- Completing a new five-year reversionary lease at Sainsburys, Torpoint with expiry moving from December 2022 to December 2027, increasing valuation by £0.2m; and

- Agreeing a five-year reversionary lease at West George Street, Glasgow with Safe Deposits Scotland, increasing valuation by £0.1m.

Rental increases of 20% have been secured on another two properties since the year end, illustrating that rental growth is taking hold. Further asset management initiatives in solicitor’s hands are expected to complete over the coming months including new lettings, lease renewals, rent reviews and lease re-gears.

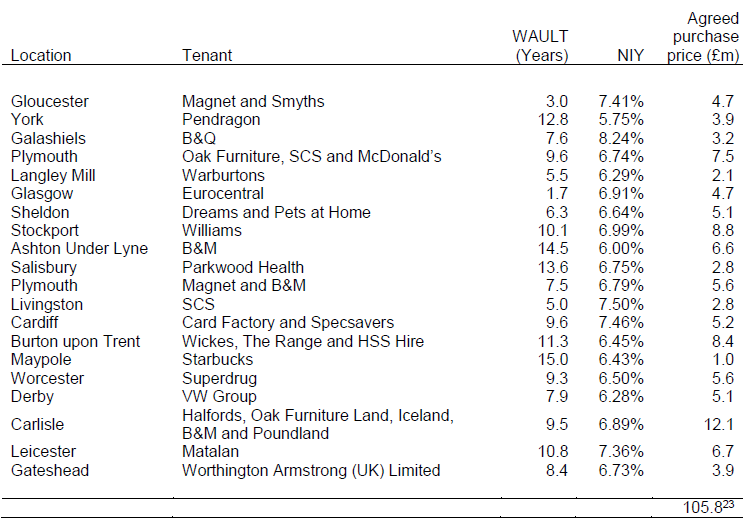

Activity

We were delighted to make the 20 acquisitions shown below. NAV has increased and the portfolio profile has strengthened in terms of diversification of tenant, sector and lease break/expiry. In addition, the portfolio’s rental growth potential has been enhanced because of these acquisitions.

A key part of effective portfolio management is the disposal of assets which either no longer meet the long-term investment strategy of the Company or which can be disposed of significantly ahead of valuation, often to a special purchaser, such that holding the asset is no longer appropriate. After focused pre-sale asset management, the following properties were sold during the Period for a total of £11.3m, realising a profit on disposal of £1.6m²⁴ at an aggregate NIY of 5.7%, with gross proceeds 20% ahead of aggregate valuation:

- An 82,081 sq ft multi-let industrial property in Chepstow for £4.6m, £0.9m ahead of valuation;

- An 8,326 sq ft retail unit in Colchester for £4.25m, £0.7m ahead of valuation;

- A 15,330 sq ft multi-tenanted industrial estate in Hinckley for £1.2m, £0.2m ahead of valuation;

- A 9,332 sq ft multi-tenanted retail parade in Redcar for £0.6m, £0.1m ahead of valuation; and

- A 10,736 sq ft retail unit in Hinckley for £0.6m, in line with valuation.

The gains made on these disposals were primarily the result of a sale to a special purchaser and the current strong market demand for regional industrial units. We intend to use the proceeds from these disposals to fund acquisitions better aligned to the Company’s long-term investment strategy.

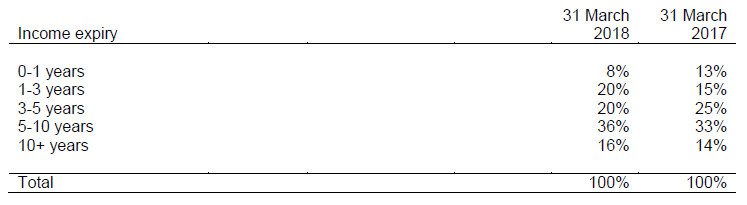

Portfolio risk

We have managed the portfolio’s income expiry profile through successful asset management activities with only 48% of income expiring within five years at 31 March 2018 (2017: 53%). Short-term income at risk is a relatively low proportion of the portfolio’s income, with only 28% expiring in the next three years (2017: 28%).

Outlook and pipeline

Looking ahead, income is likely to provide the majority of total return in the next 12-24 months. I would be disappointed if we saw further yield compression, in part because I do not think it is warranted and in larger part because I fear it may further inflate pricing bubbles in certain sectors. I believe Custodian REIT’s portfolio is insulated from the worst excesses of market pricing and I would expect Custodian REIT to have a softer landing than most should a correction occur.

The growth in the portfolio enjoyed from 2014-2017 is now showing very positive benefits to shareholders, as rental growth feeds in, ongoing charges continue to fall through economies of scale and asset management delivers further growth in NAV. The spread of income and diversification of property by sector and location that has resulted from portfolio growth stands the Company in good stead to deliver increases in fully covered dividends and to support strong shareholder total returns.

Richard Shepherd-Cross

for and on behalf of Custodian Capital Limited

Investment Manager

4 June 2018

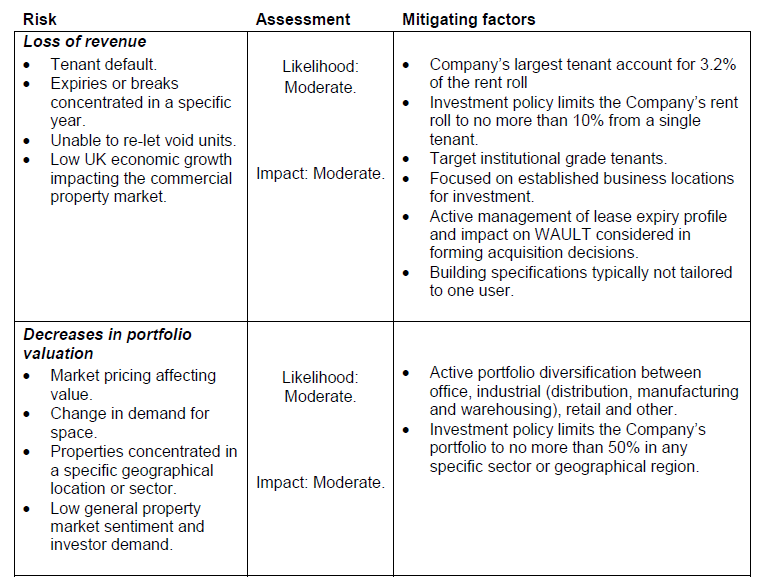

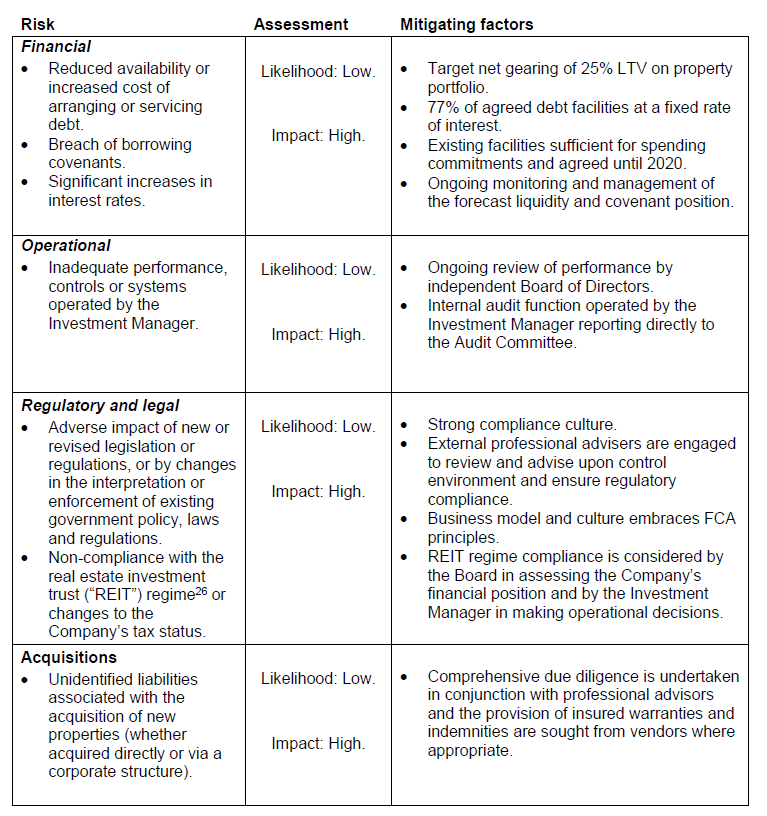

Principal risks and uncertainties

The Board has overall responsibility for reviewing the effectiveness of the system of risk management and internal control which is operated by the Investment Manager. The Company’s risk management process is designed to identify, evaluate and mitigate the significant risks the Company faces. At least annually, the Board undertakes a risk review, with the assistance of the Audit Committee, to assess the effectiveness of the Investment Manager’s risk management and internal control systems. During this review, no significant failings or weaknesses have been identified in respect of risk management, internal control and related financial and business reporting.

There are a number of potential risks and uncertainties which could have a material impact on the Company’s performance over the forthcoming financial year and could cause actual results to differ materially from expected and historical results.

The Directors have assessed the principal risks facing the Company, including those that would threaten the business model, future performance, solvency or liquidity. The table below outlines the risk factors identified, but does not purport to be exhaustive as there may be additional risks that materialise over time that the Company has not yet identified or has deemed not likely to have a potentially material adverse effect on the business.

The Board considers it is too early to understand the full impact of ‘Brexit’ on revenues and portfolio valuation, but this political risk is not considered likely to have a material impact on the Company’s performance due to the mitigating factors.

Longer-term viability statement

In accordance with provision C2.2 of the UK Corporate Governance Code issued by the Financial Reporting Council (“the Code”), the Directors have assessed the prospects of the Company over a period longer than the 12 months required by the ‘Going Concern’ provision. The Board resolved to conduct this review for a period of three years, because:

- The Company’s business plan covers a three-year period; and

- The Board believes a three-year horizon maintains a reasonable level of accuracy regarding projected rental income and costs, allowing robust sensitivity analysis to be conducted.

The Board’s three-year business plan considered the Company’s profit, cash flows, dividend cover, REIT regime compliance, borrowing covenant compliance and other key financial ratios over the period. These metrics are subject to sensitivity analysis, which involves flexing a number of key assumptions underlying the projections, including:

- Tenant default;

- Length of potential void period following lease break or expiry;

- Acquisition NIY and the timing of deployment of cash;

- Interest rate changes; and

- Property portfolio valuation movements.

This analysis also evaluates the potential impact of the principal risks and uncertainties set out above should they occur.

Current debt and associated covenants are summarised in Note 15, with no covenant breaches during the year. The Company’s dividend policy is set out in Business Model and Strategy. The principal risks and uncertainties faced by the Company, together with the steps taken to mitigate them, are highlighted above and in the Audit Committee report. The Board seeks to ensure that risks are mitigated appropriately and managed within its risk appetite all times.

Based on the results of this analysis, the Directors expect that the Company will be able to continue in operation and meet its liabilities as they fall due over the three-year period of their assessment.

Business model and strategy

Investment objective and policy

The Company seeks to provide shareholders with an attractive level of income together with the potential for capital growth from investing in a diversified portfolio of commercial real estate properties in the UK. The Company principally targets individual properties with a value of less than £10m at acquisition, seeking to benefit from a significant NIY advantage as a result.

The Company’s current investment objectives are:

- To not exceed a maximum weighting to any one property sector or to any one geographic region of greater than 50%;

- To hold a portfolio of UK commercial property, diversified by sector, location, tenant and lease term;

- To focus on areas with high residual values, strong local economies and an imbalance between supply and demand. Within these locations, the objective is to acquire modern buildings or those that are considered fit for purpose by occupiers;

- To have no one tenant or property accounting for more than 10% of the total rent roll of the portfolio at the time of purchase, except:

a) In the case of a single tenant which is a governmental body or department, where no limit shall apply; or

b) In the case of a single tenant rated by Dun & Bradstreet (“D&B”) as having a credit risk score higher than two, where the exposure to such single tenant may not exceed 5% of the total rent roll (a risk score of two represents “lower than average risk”). - To target borrowings of 25% of the aggregate market value of all the properties of the Company at the time of borrowing;

- Not to undertake speculative development (that is, development of property which has not been leased or pre-leased), save for refurbishment of existing holdings, but may (provided that it shall not exceed 20% of the gross assets of the Company) invest in forward funding agreements or forward commitments (these being arrangements by which the Company may acquire pre-development land under a structure designed to provide the Company with investment rather than development risk) of pre-let developments, where the Company intends to own the completed development; and

- To maintain a WAULT of over five years across the portfolio secured against low risk tenants and to minimise rental voids.

The Board keeps the Company’s investment objectives under review to ensure they remain appropriate to the market in which the Company operates and in the best interests of shareholders. The Board proposes amending the Company’s WAULT investment objective at the AGM as set out in the Investment Manager’s report.

Key performance indicators

The Board meets quarterly and at each meeting reviews performance against a number of key measures:

- NAV per share total return – reflects both the NAV growth of the Company and dividends paid to shareholders. The Board regards this as the best overall measure of value delivered to shareholders. The Board assesses NAV total return over various time periods and compares the Company’s returns to those of its peer group of listed, closed-ended property investment funds;

- EPRA EPS – reflects the Company’s ability to generate earnings from the portfolio which underpin dividends;

- Net gearing – measures the prudence of the Company’s financing strategy, balancing the additional returns available from employing debt with the need to effectively manage risk;

- Dividends per share and dividend cover – a key objective is to provide an attractive, sustainable level of income to shareholders, fully covered from net rental income. The Board reviews target dividends in conjunction with detailed financial forecasts to ensure that target dividends are being met and are sustainable;

- EPRA vacancy – the Board reviews the level of property voids within the Company’s portfolio on a quarterly basis and compares this to its peer group average. The Board seeks to ensure that the Investment Manager is giving proper consideration to replacing the Company’s income;

- OCR – measures the annual running costs of the Company and indicates the Board’s ability to operate the Company efficiently, keeping costs low to maximise earnings from which to pay fully covered dividends; and

- Premium or discount of the share price to NAV – the Board closely monitors the premium or discount of the share price to the NAV and believes a key driver of this is the Company’s long-term investment performance. However, there can be short-term volatility in the premium or discount and the Board therefore seeks limited authority at each AGM to issue or buy back shares with a view to trying to limit this volatility.

The Board considers the key performance measures over various time periods and against similar funds. A record of these measures is disclosed in the Financial highlights and performance summary, the Chairman’s statement and the Investment Manager’s report.

Financing

The Company operates with a conservative level of net gearing, with target borrowings over the medium-term of 25% of the aggregate market value of all properties at the time of drawdown.

Debt

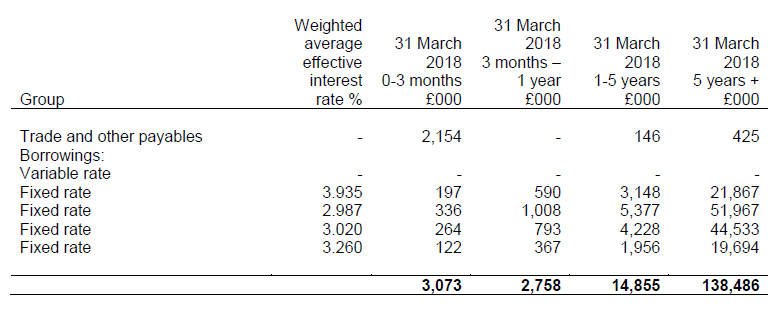

The Company has the following facilities available:

- A £35m RCF with Lloyds Bank plc attracting annual interest of 2.45% above three-month LIBOR on advances drawn down under the agreement from time to time;

- A £20m term loan facility with Scottish Widows Limited (“SWIP”) repayable in August 2025, attracting fixed annual interest of 3.935%;

- A £45m term loan facility with SWIP repayable in June 2028, attracting fixed annual interest of 2.987%; and

- A £50m term loan facility with Aviva comprising:

a) A £35m tranche repayable on 6 April 2032, attracting fixed annual interest of 3.02%; and

b) A £15m tranche repayable on 3 November 2032 attracting fixed annual interest of 3.26%.

The Company’s borrowing facilities all require minimum interest cover of 250% of the net rental income of the security pool. The maximum LTV of the Company combining the value of all property interests (including the properties secured against the facilities) must be no more than 35%.

Equity

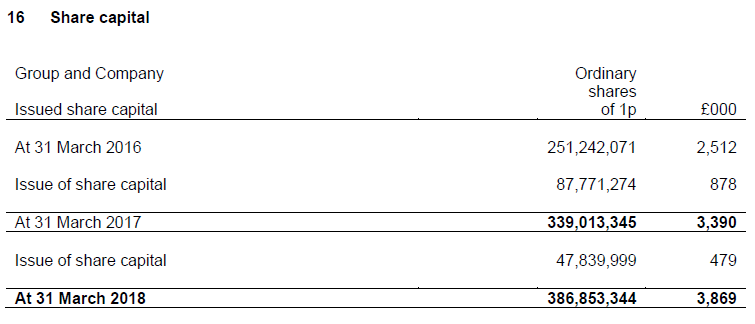

During the year the Company raised £54.7m (before costs and expenses) through the placing of 47,839,999 new ordinary shares.

Dividends

The Company paid dividends totalling 6.425p per share during the year, comprising the fourth interim dividend of 1.5875p per share relating to the year ended 31 March 2017 and three interim dividends of 1.6125p per share relating to the year ended 31 March 2018.

The Company paid an interim dividend of 1.6125p per share for the quarter ended 31 March 2018 on 31 May 2018, meeting its target of paying an annual dividend per share for the financial year of 6.45p (2017: 6.35p, 2016: 6.25p).

In the absence of unforeseen circumstances, the Board intends to pay quarterly dividends to achieve a target dividend of 6.55p per share for the year ending 31 March 2019. The Board’s objective is to grow the dividend on a sustainable basis, at a rate which is fully covered by projected net rental income and does not inhibit the flexibility of the Company’s investment strategy.

Employees

The Company has four non-executive directors and no employees. Non-executive directors are paid fixed salaries set by the Remuneration Committee and participate in the performance of the Company through their shareholdings. All non-executive directors are white males. The Board is conscious of the increased focus on diversity in the boardroom, and has constituted a Nominations Committee to ensure that for any future appointment the best person for the role is selected, while recognising the benefits of diversity when considering an appointment. The Board recognises the value and importance of diversity in the boardroom, but does not consider it appropriate or in the interests of the Company and its shareholders to set prescriptive diversity targets for the Board.

Corporate social responsibility

The Company is committed to delivering its strategic objectives in an ethical and responsible manner. The Company’s environmental and social policies address the importance of these issues in the day-to-day running of the business, as detailed below.

Environmental policy

The four key elements of the Company’s environmental policy are:

- An independent environmental report is required for all potential acquisitions, which considers, amongst other matters, the historical and current usage of the site and the extent of any contamination present;

- An ongoing examination of existing and new tenants’ business activities is carried out to assess the risk of pollution occurring. The Company monitors all incoming tenants through its insurance programme to identify potential risks and activities deemed to be high-risk are avoided. As part of the active management of the portfolio, any change in tenant business practices considered to be an environmental hazard is reported and suitably dealt with;

- Sites are visited periodically and any obvious environmental issues are reported to the Board; and

- All leases prepared after the adoption of the policy commit occupiers to observe any environmental regulations. Any problems are referred to the Board.

Social policy

The activities of the Company are carried out in a responsible manner, taking into account the social impact.

Approval of Strategic report

The Strategic report, (incorporating the Chairman’s statement, Investment Manager’s report, Portfolio, Principal risks and uncertainties and Business model and strategy) was approved by the Board of Directors and signed on its behalf by:

David Hunter

Independent Chairman

4 June 2018

Independent auditor’s report to the members of Custodian REIT plc

For the year ended 31 March 2018

We confirm that we have issued an unqualified opinion on the full financial statements of Custodian REIT plc. Our audit report on the full financial statements sets out the following key audit matters which had the greatest effect on our audit strategy; the allocation of resources in our audit; and directing the efforts of the engagement team, together with how our audit responded to those key audit matters and the key observations arising from our work:

These matters were addressed in the context of our audit of the financial statements as a whole, and in forming our opinion thereon, and we do not provide a separate opinion on these matters.

Our liability for this report, and for our full audit report on the financial statements is to the Company’s members as a body, in accordance with Chapter 3 of Part 16 of the Companies Act 2006. Our audit work has been undertaken so that we might state to the Company’s members those matters we are required to state to them in an auditor’s report and for no other purpose. To the fullest extent permitted by law, we do not accept or assume responsibility to anyone other than the Company and the Company’s members as a body, for our audit work, for our audit report or this report, or for the opinions we have formed.

Deloitte LLP

Statutory Auditor

Consolidated and Company statements of cash flows

For the year ended 31 March 2018

Notes to the financial statements for the year ended 31 March 2018

1 Corporate information

The Company is a public limited company incorporated and domiciled in England and Wales, whose shares are publicly traded on the London Stock Exchange plc’s main market for listed securities. The consolidated financial statements have been prepared on a historical cost basis, except for the revaluation of investment property, and are presented in pounds sterling with all values rounded to the nearest thousand pounds (£000), except when otherwise indicated. The consolidated financial statements were authorised for issue in accordance with a resolution of the Directors on 4 June 2018.

2 Basis of preparation and accounting policies

2.1. Basis of preparation

The consolidated financial statements and the separate financial statements of the parent company have been prepared in accordance with International Financial Reporting Standards adopted by the International Accounting Standards Board (“IASB”) and interpretations issued by the International Financial Reporting Interpretations Committee (“IFRIC”) of the IASB (together “IFRS”) as adopted by the European Union, and in accordance with the requirements of the Companies Act applicable to companies reporting under IFRS, and therefore they comply with Article 4 of the EU IAS Regulation.

Certain statements in this report are forward looking statements. By their nature, forward looking statements involve a number of risks, uncertainties or assumptions that could cause actual results or events to differ materially from those expressed or implied by those statements. Forward looking statements regarding past trends or activities should not be taken as representation that such trends or activities will continue in the future. Accordingly, undue reliance should not be placed on forward looking statements.

2.2. Basis of consolidation

The consolidated financial statements consolidate those of the parent company and its subsidiaries. The parent controls a subsidiary if it is exposed, or has rights, to variable returns from its involvement with the subsidiary and has the ability to affect those returns through its power over the subsidiary. Custodian Real Estate Limited has a reporting date in line with the Company. Other subsidiaries have a December or June accounting reference date which has not been amended since their acquisition as those companies are expected to be liquidated during the next financial year. All transactions and balances between group companies are eliminated on consolidation, including unrealised gains and losses on transactions between group companies. Where unrealised losses on intra-group asset sales are reversed on consolidation, the underlying asset is also tested for impairment from a group perspective. Amounts reported in the financial statements of the subsidiary are adjusted where necessary to ensure consistency with the accounting policies adopted by the Group. Profit or loss and other comprehensive income of subsidiaries acquired or disposed of during the year are recognised from the effective date of acquisition, or up to the effective date of disposal, as applicable.

2.3. Application of new and revised International Financial Reporting Standards

During the year the Company has applied a number of amendments to IFRSs and a new interpretation issued by the International Accounting Standards Board (IASB) that are mandatorily effective for accounting periods beginning on or after 1 April 2017:

- Annual Improvements to IFRSs 2014-2016 Cycle and;

- Amendments to IAS 7 ‘Disclosure initiative’.

The Company adopted the amendments to IAS 7 for the first time during the year which require disclosure to enable the users of the financial statements to evaluate changes in liabilities arising from financing activities. Borrowings are the Company’s only liabilities arising from financing activities and a reconciliation between opening and closing balances is shown in Note 15. The application of these new standards has otherwise had no impact on the disclosures or on the amounts recognised in the Company’s financial statements.

At the date of authorisation of these financial statements, the following new and revised IFRSs which have not been applied in these financial statements were in issue but not yet effective:

- Annual Improvements to IFRSs 2015-2017 Cycle;

- IFRS 9 ‘Financial Instruments’;

- IFRS 15 ‘Revenue from Contracts with Customers’;

- IFRS 16 ‘Leases’; and

- IFRS 17 ‘Insurance Contracts’

IFRS 9

IFRS 9 ‘Financial instruments’ was issued in July 2014, and the new standard is effective for accounting periods beginning on or after 1 January 2018 and will be adopted by the Company on 1 April 2018. IFRS 9 was adopted by the EU in November 2016.

IFRS 9 introduces changes to the classification of financial assets and a new impairment model for financial assets, which could impact the timing of recognition of impairment losses. Under the ‘simplified approach’ to the expected credit loss model, loss allowances equal to the lifetime expected credit losses are recognised on initial recognition of financial assets, depending on assessed credit risk. Additional requirements include both quantitative and qualitative disclosures supporting the basis and recognition of loss allowances, and the recognition of the loss allowance within provisions.

The Company is assessing the impact of the following accounting changes that will arise under IFRS 9:

- Classification of financial assets held by the Company is not expected to change.

- Provisions for impairment losses against financial assets could be recognised sooner as lifetime expected credit losses are recognised on initial recognition of those financial assets.

- The Company’s trade receivables, other receivables and accrued income are short-term and do not include a financing component, therefore the Company expects to apply the simplified approach and reflect lifetime credit losses.

The Company will apply IFRS 9 from 1 April 2018 and has elected not to restate comparatives on initial application of IFRS 9. The full impact of adopting IFRS 9 on the Company’s financial statements will depend on the financial instruments that the Company has during 2018 as well as on economic conditions and judgements made as at the year end.

Based on the Company’s credit losses incurred in the current and preceding financial years, the expected additional provision to be recognised is £nil.

IFRS 15

IFRS 15 ‘Revenue from contracts with customers’ was issued in May 2014, and the new standard is effective for accounting periods beginning on or after 1 January 2018 and will be adopted by the Company on 1 April 2018. IFRS 15 was adopted by the EU in October 2016.

IFRS 15 will change the way revenue from customer contracts is recognised, potentially impacting both the timing at which revenue may be recognised, and the value of revenue recognised. Customer contracts are broken down in to separate performance obligations, with contractual revenues being allocated to each performance obligation and revenue recognised on a basis consistent with the transfer of control of goods or services. Additional disclosure requirements include the reporting of disaggregated revenues, and the recognition of contract assets and contract liabilities on the face of the statement of financial position.

The Company is assessing the impact of the accounting and disclosure changes that will arise under IFRS 15 and at present only anticipates a minimal impact on revenue recognition and reported net assets due to certain leases containing an element of variable consideration.

IFRS 16

IFRS 16 ‘Leases’ was issued in January 2016 and is effective for accounting periods beginning on or after 1 January 2019 and will be adopted by the Company on 1 April 2019.

IFRS 16 removes the distinction between operating and finance leases for lessees and replaces them with the concept of ‘right-of-use’ assets and associated financial liabilities which will result in almost all leases being recognised on the balance sheet. A leasee’s rent expense under IAS 17 for operating leases will be removed and replaced with depreciation and finance costs.

Additional disclosure requirements include presenting:

- Depreciation expense

- Carrying value of right-of-use assets

- Additions to right-of-use assets

- Interest expense on lease liabilities

- Variable lease payments not included in the lease liability

- Total cash outflow for leases

Additional qualitative and quantitative disclosures will also be necessary about the entity’s leasing activities if they are considered necessary to meet the overall disclosure objective.

The Company is assessing the impact of the accounting and disclosure changes that will arise under IFRS 16 and at present only anticipates a £0.03m impact on income statement categorisation of headlease costs, with no impact on bank covenants.

IFRS 17

IFRS 17 was published in May 2017 and is effective for periods commencing on or after 1 January 2021. The Company has not completed its review of the impact of this new standard but does not anticipate it having a significant impact.

2.4. Significant accounting policies

The principal accounting policies adopted by the Group and Company and applied to these financial statements are set out below.

Going concern

The Directors believe the Company is well placed to manage its business risks successfully. The Company’s projections show that the Company should continue to be cash generative and be able to operate within the level of its current financing arrangements. Accordingly, the Directors continue to adopt the going concern basis for the preparation of the financial statements.

Income recognition

Revenue is recognised to the extent that it is probable that economic benefits will flow to the Company and the revenue can be reliably measured. Revenue is measured at the fair value of the consideration received, excluding discounts, rebates, VAT and other sales taxes or duties.

Rental income from operating leases on properties owned by the Company is accounted for on a straight line basis over the term of the lease. Rental income excludes service charges and other costs directly recoverable from tenants.

Lease incentives are recognised on a straight-line basis over the lease term.

Revenue and profits on the sale of properties are recognised on the completion of contracts. The amount of profit recognised is the difference between the sale proceeds and the carrying amount.

Finance income relates to bank interest receivable and amounts receivable on ongoing development funding contracts.

Taxation

The Group operates as a REIT and hence profits and gains from the property rental business are normally expected to be exempt from corporation tax. The tax expense represents the sum of the tax currently payable and deferred tax relating to the residual (non-property rental) business. The tax currently payable is based on taxable profit for the year. Taxable profit differs from net profit as reported in the statement of comprehensive income because it excludes items of income and expense that are taxable or deductible in other years and it further excludes items that are never taxable or deductible. The Company’s liability for current tax is calculated using tax rates that have been enacted or substantively enacted by the reporting date.

Investment property

Investment property is held to earn rentals and/or for capital appreciation and is initially recognised at cost including direct transaction costs. Investment property is subsequently valued externally on a market basis at the reporting date and recorded at valuation. Any surplus or deficit arising on revaluing investment property is recognised in profit or loss in the year in which it arises. Dilapidations receipts are held in the statement of financial position and offset against subsequent associated expenditure. Any ultimate gains or shortfalls are measured by reference to previously published valuations and recognised in profit or loss, offset against any directly corresponding movement in fair value of the investment properties to which they relate.

Group undertakings

Investments are included in the Company only statement of financial position at cost less any provision for impairment.

Financial assets

The Company’s financial assets include cash and cash equivalents and trade and other receivables. All financial assets are initially recognised at fair value plus transaction costs, when the Company becomes party to the contractual provisions of the instrument. Interest resulting from holding financial assets is recognised in profit or loss on an accruals basis.

Loans and receivables are measured subsequent to initial recognition at amortised cost using the effective interest method, less provision for impairment. Provision for impairment of trade and other receivables is made when objective evidence is received that the Company will not be able to collect all amounts due to it in accordance with the original terms of the receivable. The amount of the impairment is determined as the difference between the asset’s carrying amount and the present value of estimated future cash flows, discounted at the effective rate computed at initial recognition. Any change in value through impairment or reversal of impairment is recognised in profit or loss.

A financial asset is derecognised only where the contractual rights to the cash flows from the asset expire or the financial asset is transferred and that transfer qualifies for de-recognition. A financial asset is transferred if the contractual rights to receive the cash flows of the asset have been transferred or the Company retains the contractual rights to receive the cash flows of the asset but assumes a contractual obligation to pay the cash flows to one or more recipients. A financial asset that is transferred qualifies for de-recognition if the Company transfers substantially all the risks and rewards of ownership of the asset.

Cash and cash equivalents

Cash and cash equivalents include cash in hand and on-demand deposits, and other short-term highly liquid investments that are readily convertible into a known amount of cash and are subject to an insignificant risk of changes in value.

Cash proceeds held in charged bank accounts from the disposal of investment property on which bank borrowings are secured is recognised within other receivables.

Financial liabilities and equity

Financial liabilities and equity instruments are classified according to the substance of the contractual arrangements entered into. An equity instrument is any contract that evidences a residual interest in the assets of the Company after deducting all of its liabilities. Equity instruments issued by the Company are recorded at the proceeds received, net of direct issue costs.

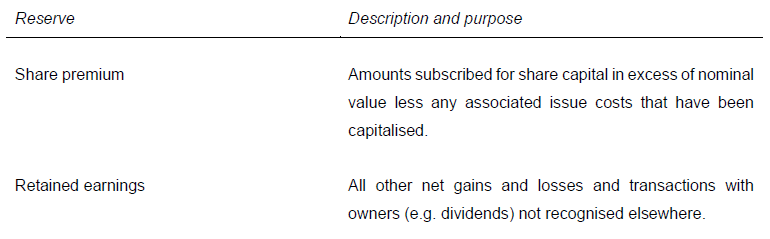

Share capital represents the nominal value of equity shares issued. Share premium represents the excess over nominal value of the fair value of the consideration received for equity shares, net of direct issue costs.

Retained earnings include all current and prior year results as disclosed in profit or loss. Retained earnings include realised and unrealised profits. Profits are considered unrealised where they arise from movements in the fair value of investment properties that are considered to be temporary rather than permanent.

Bank borrowings

Interest-bearing bank loans and overdrafts are recorded at the fair value of proceeds received, net of direct issue costs. Finance charges, including premiums payable on settlements or redemption and direct issue costs, are accounted for on an accruals basis in profit or loss using the effective interest rate method and are added to the carrying amount of the instrument to the extent that they are not settled in the period in which they arise.

Trade payables

Trade payables are initially measured at fair value and are subsequently measured at amortised cost, using the effective interest rate method.

Leases

Payments on operating lease agreements where the Company is lessor are recognised as an expense on a straight-line basis over the lease term. Payments on operating lease agreements where the Company is lessee are charged to profit or loss on a straight-line basis over the term of the lease.

Segmental reporting

An operating segment is a distinguishable component of the Company that engages in business activities from which it may earn revenues and incur expenses, whose operating results are regularly reviewed by the Company’s chief operating decision maker (the Board) to make decisions about the allocation of resources and assessment of performance and about which discrete financial information is available. As the chief operating decision maker reviews financial information for, and makes decisions about the Company’s investment properties as a portfolio, the Directors have identified a single operating segment, that of investment in commercial properties.

2.5. Key sources of judgements and estimation uncertainty

The preparation of the financial statements requires the Company to make estimates and assumptions that affect the reported amount of revenues, expenses, assets and liabilities and the disclosure of contingent liabilities. If in the future such estimates and assumptions, which are based on the Directors’ best judgement at the date of preparation of the financial statements, deviate from actual circumstances, the original estimates and assumptions will be modified as appropriate in the period in which the circumstances change.

Judgements

The areas where a higher degree of judgement or complexity arises are discussed below.

- Valuation of property – Investment property is valued at the reporting date at fair value. Where an investment property is being redeveloped the property continues to be treated as an investment property. Surpluses and deficits attributable to the Company arising from revaluation are recognised in profit or loss. Valuation surpluses reflected in retained earnings are not distributable until realised on sale. In making its judgement over the valuation of properties, the Company considers valuations performed by the independent valuer in determining the fair value of its investment properties. The valuations are based upon assumptions including future rental income, anticipated maintenance costs and appropriate discount rates. The valuer also makes reference to market evidence of transaction prices for similar properties.

- Acquisition of subsidiaries – The Board applies judgement as to whether the acquisition of a subsidiary comprises an asset purchase or a business combination²⁷. A business comprises an integrated set of activities, including strategic and operational management, and assets capable of being managed for the purpose of providing an economic benefit to the owner. The Board assessed the acquisition of subsidiaries detailed in Note 11 as an asset purchase because all outsourced strategic and operational management contracts were terminated on acquisition.

Estimates

There are no areas where assumptions and estimates are significant to the financial statements.

2.6. Change in accounting presentation

During the year the classification of deferred lease incentives has been reviewed and compared with industry peers, resulting in a presentational change with no impact on total return or NAV. These assets were previously reported as a separate receivable and deducted from the independent property valuation in arriving at the reported investment property balance. To align the Company’s accounting presentation with that adopted by many industry peers, assets totalling £2.7m at 31 March 2017 and £1.5m at 31 March 2016 have been reclassified from receivables to investment property in retrospectively restating the statement of financial position and the associated notes at those dates in these financial statements.

3 Earnings per ordinary share

Basic EPS amounts are calculated by dividing net profit for the year attributable to ordinary equity holders of the Company by the weighted average number of ordinary shares outstanding during the year.

Diluted EPS amounts are calculated by dividing the net profit attributable to ordinary equity holders of the Company by the weighted average number of ordinary shares outstanding during the year plus the weighted average number of ordinary shares that would be issued on the conversion of all the dilutive potential ordinary shares into ordinary shares. There are no dilutive instruments in issue. Shares issued after the year end are disclosed in Note 20.

The Company became a FTSE EPRA/NAREIT index series constituent in March 2017 and EPRA performance measures have been disclosed to facilitate comparability with the Company’s peers through consistent reporting of key performance measures. EPRA has issued recommended bases for the calculation of EPS which the Directors consider are better indicators of performance.

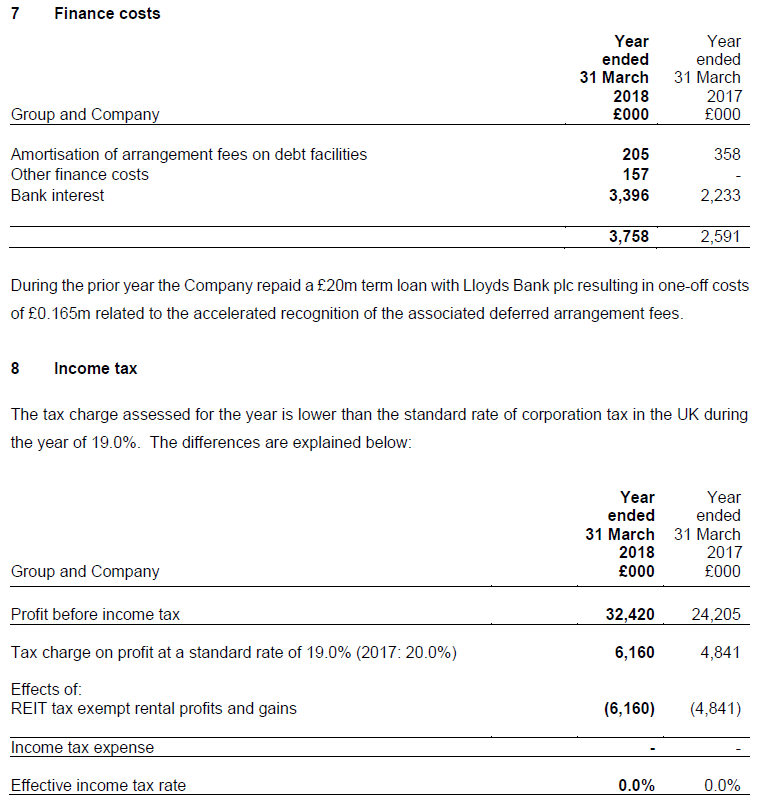

The Company operates as a REIT and hence profits and gains from the property investment business are normally exempt from corporation tax. Reductions in the UK corporation tax rate from 20% to 19% (effective from 1 April 2017) and to 17% (effective 1 April 2020) were substantively enacted at 6 September 2016.

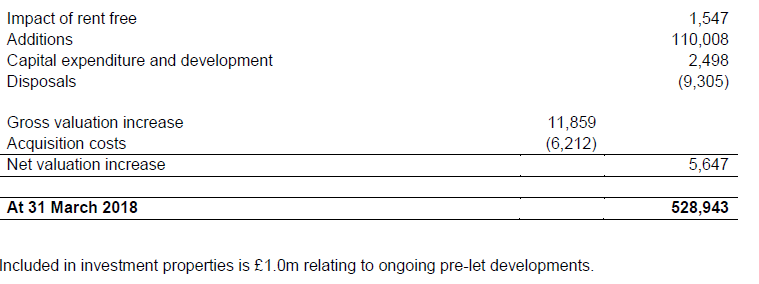

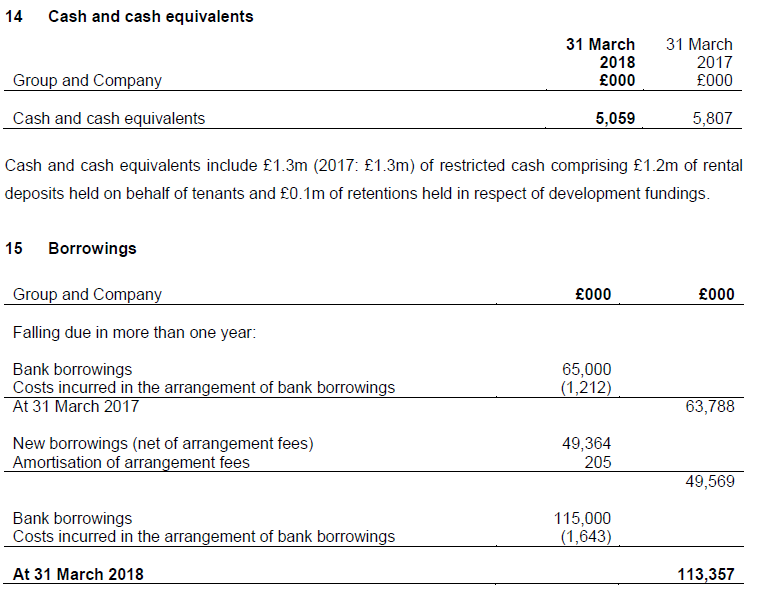

£362.8m (2017: £233.1m) of investment property has been charged as security against the Company’s borrowings.

The carrying value of investment property at 31 March 2018 comprises £459.8m freehold (2017: £361.6m) and £69.1m leasehold property (2017: £54.2m)

Investment property is stated at the Directors’ estimate of its 31 March 2018 fair value. Lambert Smith Hampton Group Limited (“LSH”), a professionally qualified independent valuer, valued the property as at 31 March 2018 in accordance with the Appraisal and Valuation Standards published by the Royal Institution of Chartered Surveyors. LSH has recent experience in the relevant location and category of the property being valued.

Investment property has been valued using the investment method which involves applying a yield to rental income streams. Inputs include yield, current rent and ERV. For the year end valuation, the equivalent yields used ranged from 4.7% to 9.0%. Valuation reports are based on both information provided by the Company e.g. current rents and lease terms, which are derived from the Company’s financial and property management systems and are subject to the Company’s overall control environment, and assumptions applied by the valuer e.g. ERVs and yields. These assumptions are based on market observation and the valuer’s professional judgement. In estimating the fair value of each property, the highest and best use of the properties is their current use.

All other factors being equal, a higher equivalent yield would lead to a decrease in the valuation of investment property, and an increase in the current or estimated future rental stream would have the effect of increasing capital value, and vice versa. However, there are interrelationships between unobservable inputs which are partially determined by market conditions, which could impact on these changes.

Investment property additions include £6.7m relating to the purchase of a retail warehouse in Leicester, which the Company acquired by purchasing the entire issued share capital of Custodian Real Estate BL Limited (formerly BL (Leicester) Limited), the immediate parent of Custodian Real Estate (Beaumont Leys) Limited (formerly Belgrave Land (Beaumont Leys) Limited) and Custodian Real Estate (Leicester) Limited (formerly Belgrave Land (Leicester) Limited), which held the title and beneficial interest in the property on acquisition.

On 15 March 2018 the trade and assets of Custodian Real Estate (Beaumont Leys) Limited and Custodian Real Estate (Leicester) Limited were transferred to the Company at cost, which was considered market value.

11 Investments

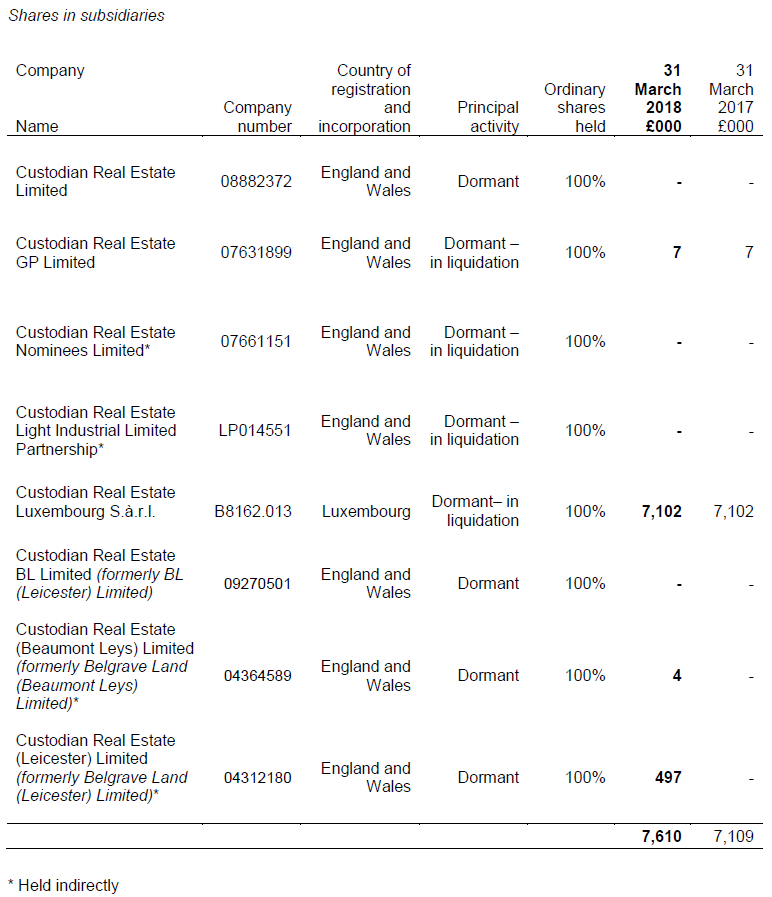

The Company’s dormant UK subsidiaries have claimed the audit exemption available under Section 479A of the Companies Act 2006. The Company’s registered office is also the registered office of each UK subsidiary. The registered office of Custodian Real Estate Luxembourg S.à.r.l. is 2 Rue d’Alsace, L-1122, Luxembourg.

The Company acquired 100% of the ordinary share capital of Custodian Real Estate BL Limited on 21 December 2017. Custodian Real Estate BL Limited owns 100% of the ordinary share capital of Custodian Real Estate (Beaumont Leys) Limited and Custodian Real Estate (Leicester) Limited.

The Company acquired 100% of the ordinary share capital of Custodian Real Estate GP Limited and Custodian Real Estate Luxembourg S.à.r.l. on 29 September 2016 as part of the acquisition of the Light Industrial Portfolio. Custodian Real Estate GP Limited owns 100% of the ordinary share capital of Custodian Real Estate Nominees Limited. Custodian Real Estate Luxembourg S.à.r.l. and Custodian Real Estate GP Limited hold 99.9% and 0.1% beneficial interests respectively in Custodian Real Estate Light Industrial Limited Partnership.

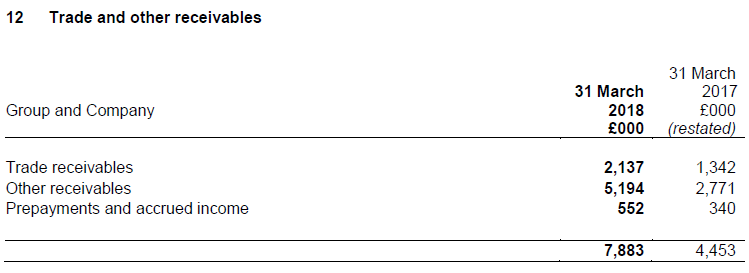

The Company has provided fully for those receivable balances that it does not expect to recover. This assessment has been undertaken by reviewing the status of all significant balances that are past due and involves assessing both the reason for non-payment and the creditworthiness of the counterparty. Trade receivables include £0.2m (2017: £0.1m) which are past due as at 31 March 2018 for which no provision has been made because the amounts are considered recoverable.

Included in other receivables is £4.4m cash proceeds held in charged bank accounts from the disposal of investment property on which bank borrowings are secured.

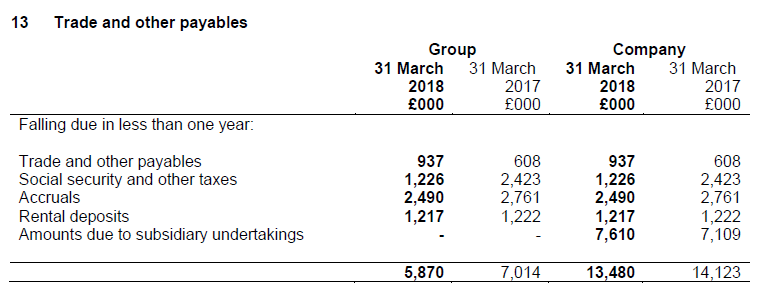

The Directors consider that the carrying amount of trade and other payables approximates to their fair value. Trade payables and accruals principally comprise amounts outstanding for trade purchases and ongoing costs. For most suppliers interest is charged if payment is not made within the required terms. Thereafter, interest is chargeable on the outstanding balances at various rates. The Company has financial risk management policies in place to ensure that all payables are paid within the credit timescale.

Amounts payable to subsidiary undertakings, arising on the transfer of the trade and assets of Custodian Real Estate Light Industrial Limited Partnership to the Company, are due on demand.

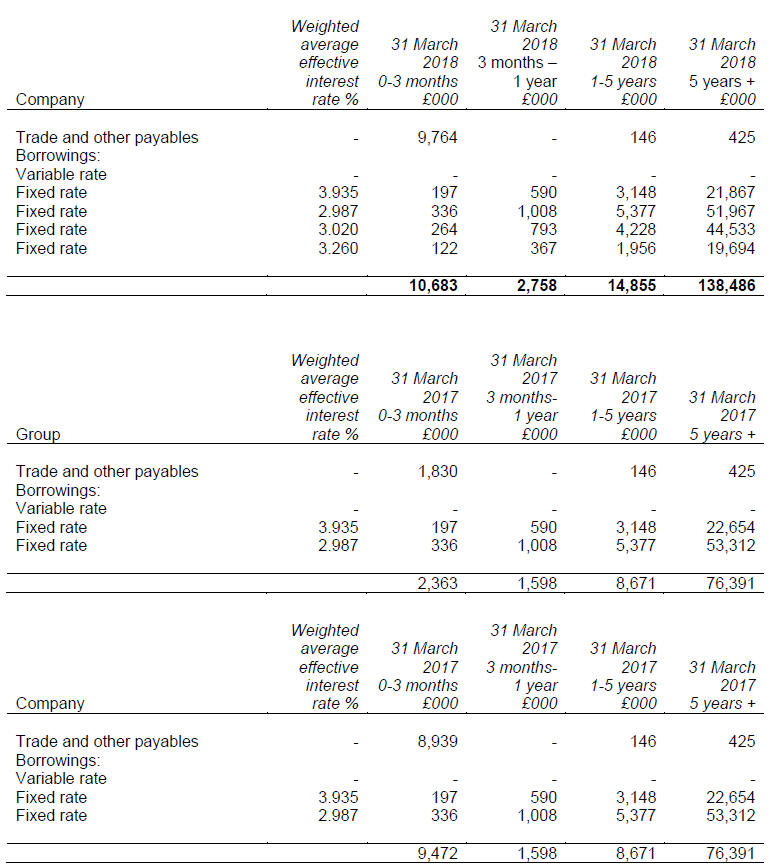

The Company has the following facilities available:

- A £35m RCF with Lloyds Bank plc attracting annual interest of 2.45% above three-month LIBOR on advances drawn down under the agreement from time to time;

- A £20m term loan facility with Scottish Widows Limited (“SWIP”) repayable in August 2025, attracting fixed annual interest of 3.935%;

- A £45m term loan facility with SWIP repayable in June 2028, attracting fixed annual interest of 2.987%; and

- A £50m term loan facility with Aviva comprising:

c) A £35m tranche repayable on 6 April 2032, attracting fixed annual interest of 3.02%; and

d) A £15m tranche repayable on 3 November 2032 attracting fixed annual interest of 3.26%.

The RCF was not drawn at the year end.

All of the Company’s borrowing facilities require minimum interest cover of 250% of the net rental income of the security pool. The maximum LTV of the Company combining the value of all property interests (including the properties secured against the facilities) must be no more than 35%.

During the year, the Company raised £54.7m (before costs and expenses) through the placing of 47,839,999 new ordinary shares.

Rights, preferences and restrictions on shares

All ordinary shares carry equal rights and no privileges are attached to any shares in the Company. All the shares are freely transferable, except as otherwise provided by law. The holders of ordinary shares are entitled to receive dividends as declared from time to time and are entitled to one vote per share at meetings of the Company. All shares rank equally with regard to the Company’s residual assets.

At the AGM of the Company held on 20 July 2017, the Board was given authority to issue up to 115,171,100 shares, pursuant to section 551 of the Companies Act 2006. This authority is intended to satisfy market demand for the ordinary shares and raise further monies for investment in accordance with the Company’s investment policy. 38,999,999 ordinary shares have been issued under this authority since 20 July 2017, leaving an unissued balance of 76,171,001 at 31 March 2018.

In addition, the Company was granted authority to make market purchases of up to 34,551,334 ordinary shares under section 701 of the Companies Act 2006. No market purchases of ordinary shares have been made.

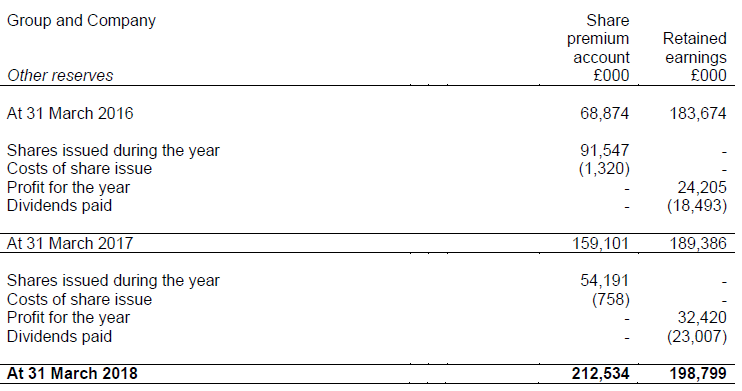

The following table describes the nature and purpose of each reserve within equity:

17 Commitments and contingencies

Company as lessor

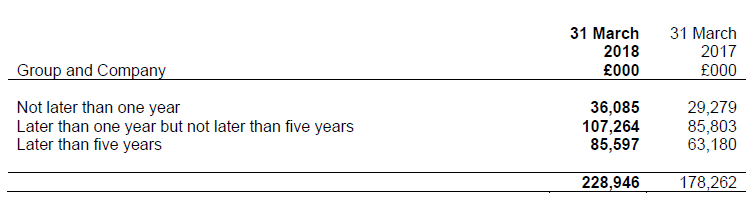

The Company lets all investment properties under operating leases. The aggregated future minimum rentals receivable under all non-cancellable operating leases are:

Company as lessee

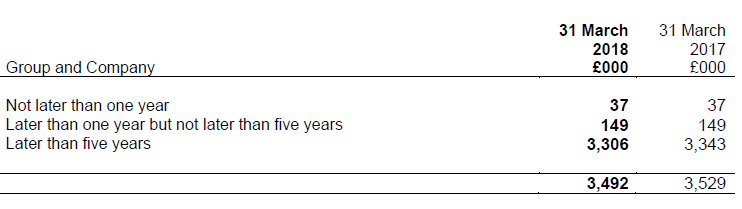

The Company owns long-leasehold property and has non-cancellable payments due under headlease liabilities of:

18 Related party transactions

Save for transactions described below, the Company is not a party to, nor had any interest in, any other related party transaction during the year.

Transactions with directors

Each of the directors is engaged under a letter of appointment with the Company and does not have a service contract with the Company. Under the terms of their appointment, each director is required to retire by rotation and seek re-election at least every three years. Each director’s appointment under their respective letter of appointment is terminable immediately by either party (the Company or the director) giving written notice and no compensation or benefits are payable upon termination of office as a director of the Company becoming effective.

Ian Mattioli is Chief Executive of Mattioli Woods, the parent company of the Investment Manager, and is a director of the Investment Manager. As a result, Ian Mattioli is not independent. The Company Secretary, Nathan Imlach, is also a director of Mattioli Woods and the Investment Manager.

Investment Management Agreement

On 25 February 2014 the Company entered into a three-year IMA with the Investment Manager commencing on Admission, under which the Investment Manager was appointed as AIFM with responsibility for the property management of the Company’s assets, subject to the overall supervision of the Directors. The Investment Manager manages the Company’s investments in accordance with the policies laid down by the Board and the investment restrictions referred to in the IMA. The Investment Manager also provides day-to-day administration of the Company and acts as secretary to the Company, including maintenance of accounting records and preparing the annual financial statements of the Company.

On 1 June 2017 the terms of the IMA were varied with effect from that date to extend the appointment of the Investment Manager for a further three years and to introduce further fee hurdles such that annual management fees payable to the Investment Manager under the IMA are: